Most guides on stablecoin lending rates read like a shopping list: here are the platforms, here are the rates, now diversify and use a dashboard. That framing quietly misses the one thing that actually matters. A stablecoin lending rate is not a price someone quotes you — it is the output of a formula, recalculated block by block from a single input. Understand that formula and you understand everything: why the rate jumps, why a tempting yield is usually a warning, and why a transparent on-chain rate is safer than a fixed promise from a lender you can't see inside.

So this piece isn't a leaderboard of yields. It's a look under the hood at the mechanism that sets the rate, and at the two risks that mechanism is quietly telling you about — the risk you can read on-chain, and the opaque kind that bankrupted a generation of centralized lenders.

Nobody Sets the Rate

On a decentralized lending protocol, no committee decides today's USDC rate. Lenders deposit into a shared pool, borrowers draw from it, and a smart contract adjusts the interest rate automatically to keep the two in balance. When borrowing is light relative to deposits, the rate falls to attract borrowers; when borrowing is heavy, the rate climbs to attract new deposits and encourage repayment. The rate is simply the market clearing itself, in public, in real time.

That single design choice is why DeFi lending behaves so differently from a bank account. There is no promised APY, because there is nothing to promise — the number you see is whatever the pool's current balance produces. That same honesty is exactly what a headline staking or yield-farming APY usually hides. To see why that's actually a feature rather than a flaw, it helps to understand how DeFi rebuilds lending without a bank in the middle.

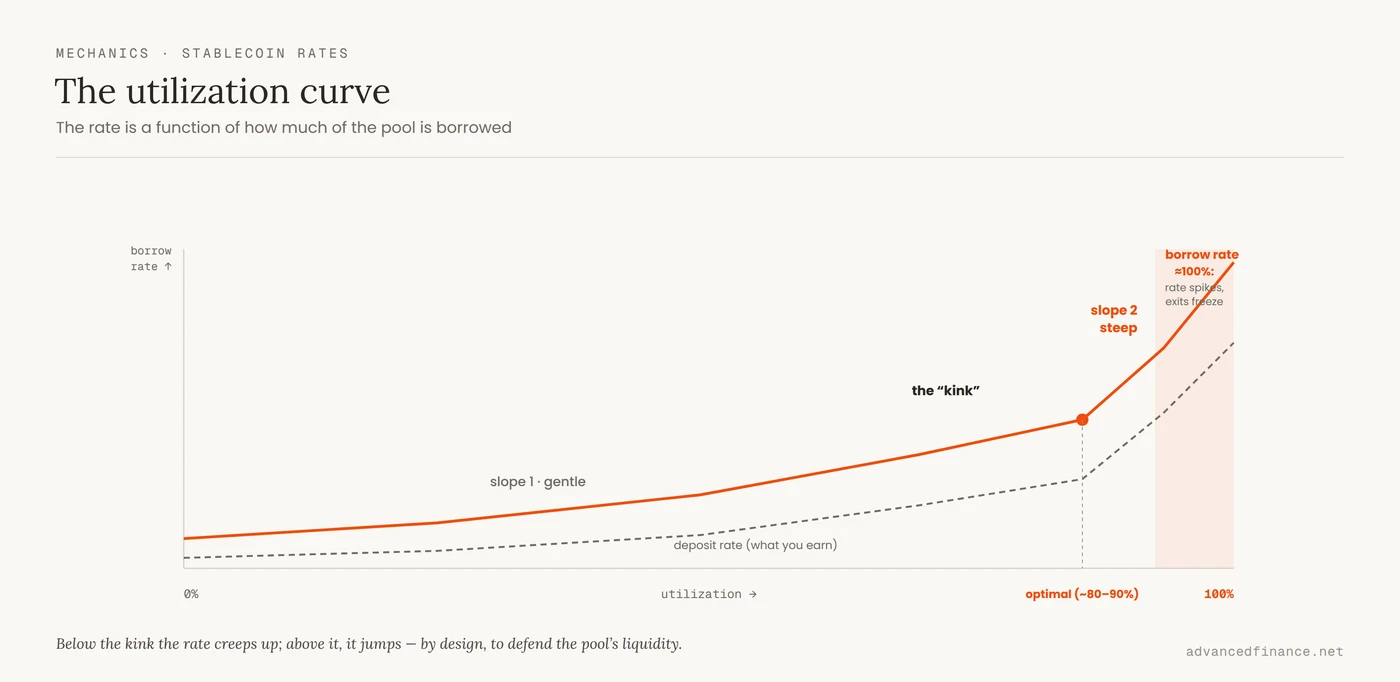

The Utilization Curve

The single input driving the whole thing is utilization — the share of the pool that's currently borrowed. If $100 is deposited and $80 is borrowed, utilization is 80%. Every major protocol maps utilization to an interest rate through a published curve, and the shape of that curve is the most important thing you can learn about a lending market.

The curve has a deliberate bend in it, usually called the "kink" or optimal point. Below that point, the rate rises gently as utilization climbs. Above it, the rate rises steeply — a sharp penalty designed to pull the pool back toward a healthy balance. This isn't proprietary or hidden: Aave publishes its exact interest-rate strategy, with the optimal-utilization point and the two slopes, in its documentation (Aave), and Compound does the same for its markets (Compound). You can read the formula that will set your rate before you deposit a cent.

The formula itself is simple. Below the kink, the borrow rate rises gently with utilization; above it, a second, much steeper slope takes over:

Below optimal: borrow rate = base + (utilization ÷ optimal) × slope₁

Above optimal: borrow rate = base + slope₁ + ((utilization − optimal) ÷ (1 − optimal)) × slope₂

For major stablecoin markets the optimal point is usually set high — often around 80–90% — and it, together with the two slopes, is a governance parameter you can look up rather than a fixed law.

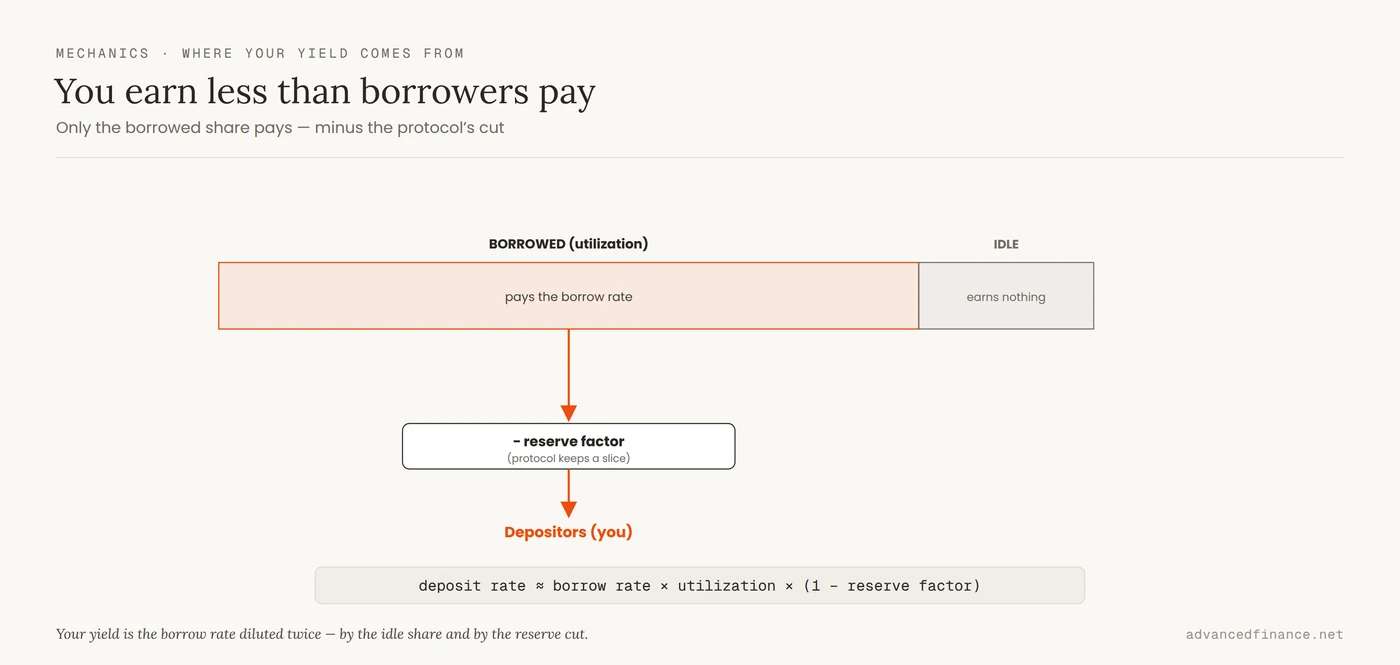

One more piece closes the loop, and it's the one most yield-chasers miss: what you earn as a lender is not the borrow rate. Only the borrowed portion of the pool pays interest, and the protocol keeps a slice (the "reserve factor"), so your deposit yield is roughly:

deposit rate ≈ borrow rate × utilization × (1 − reserve factor)

That's why the APY you're offered always sits below the rate borrowers pay — and why utilization is doing double duty: it sets the borrow rate and scales how much of that rate actually reaches you.

| Utilization | What it means | Rate behaviour |

|---|---|---|

| Low | Plenty of idle supply, few borrowers | Rate is low; easy to withdraw |

| Near the "kink" (optimal) | Pool is working efficiently | Rate moderate; the intended balance |

| High (past the kink) | Most supply is lent out | Rate climbs steeply to attract deposits |

| ~100% | Almost nothing left to withdraw | Rate spikes; exits may be blocked until borrowers repay |

High Yield Is a Risk Signal

Here's the reframe that changes how you lend: a high stablecoin rate is not a gift, it's a message. Because the rate is a function of utilization, an unusually high yield almost always means the pool is heavily borrowed — which is exactly the moment your capital is least available and most exposed. The market isn't rewarding you for being clever; it's paying you more because you're taking more risk, and it's telling you so out loud.

This is the same logic behind where a DeFi yield actually comes from: a sustainable rate is paid by real borrowers who need the capital, while a suspiciously high one is often a sign of stress, thin liquidity, or a subsidy that won't last. Before chasing a number, ask what utilization it corresponds to — and treat "too good to be true" as a prompt to spot a yield that's too good to be true before you commit.

When You Can't Withdraw

The risk the utilization curve is really warning about isn't rate volatility — it's liquidity. When utilization approaches 100%, almost every deposited dollar is out on loan, and there simply isn't cash in the pool for you to withdraw. Your funds aren't lost; they're locked until borrowers repay or new lenders arrive, drawn in by the spiking rate. But if you needed that money during a market panic — precisely when utilization tends to max out — "locked until later" can feel a lot like "gone."

This is why reading the current utilization matters more than reading the headline yield. A 6% rate at 70% utilization is a very different proposition from a 12% rate at 99% utilization, even though the second looks better on a dashboard. The first is a market doing its job; the second is a warning light. Always check whether you can actually exit before you're seduced by the rate.

The Opaque-Yield Trap

Now contrast all of that transparency with how centralized lenders worked. Platforms like BlockFi and Celsius advertised fixed, generous stablecoin yields — no utilization curve to read, no on-chain pool to inspect, just a number and a promise. The obvious question, the one the DeFi model forces you to ask, was impossible to answer: where is this yield actually coming from?

The answer, it turned out, was hidden risk. These firms took customer deposits and lent or invested them opaquely, and when those bets soured, depositors were wiped out. Both collapsed into bankruptcy in 2022; U.S. regulators later took action, with the SEC penalizing BlockFi over its lending product (SEC) and the FTC settling with Celsius over "duping consumers" and squandering billions in deposits (FTC). The lesson isn't "CeFi bad, DeFi good" — on-chain protocols carry their own smart-contract and depeg risks. It's that a yield you can't trace to a mechanism is a yield you can't trust, and it helps to know how a stablecoin holds its peg before you lend it anywhere.

| Question | Transparent (on-chain DeFi) | Opaque (CeFi promise) |

|---|---|---|

| Who sets the rate? | A published formula on utilization | The company, at its discretion |

| Where's the yield from? | Visible borrower demand in the pool | Undisclosed lending or bets |

| Can you verify it? | Yes, on-chain in real time | No — you trust a statement |

How to Read a Rate

Put the mechanism to work with a short routine before you lend a single stablecoin. First, look up the pool's current utilization, not just its rate — that one number tells you both your likely yield and your exit risk. Second, glance at the protocol's rate curve so you know how fast the rate (and utilization pressure) can move against you. Third, ask the question CeFi couldn't answer: who is paying this yield, and is it real borrower demand or a temporary incentive? Fourth, size the position so that funds being briefly locked at peak utilization would be an inconvenience, not a crisis.

You don't need a paid service for any of this. DeFiLlama and each protocol's own market screen show current utilization and both rates side by side, and a block explorer like Etherscan exposes the raw on-chain values if you want to verify them yourself. The same read works across the major venues — Aave, Compound, and newer markets such as Morpho, Spark, and Sky — but rates move constantly and differ by chain and by stablecoin, so compare them live rather than trusting any figure you saw last week.

None of this requires a robo-advisor. It requires reading the two numbers — rate and utilization — that every transparent protocol already shows you, and refusing to lend where you can't see them at all.

FAQ

What actually determines a stablecoin lending rate?

One number: utilization, the share of the pool that's borrowed. A smart contract maps utilization to a rate along a published curve, so the borrow rate is a live output of the formula rather than a figure anyone quotes. Below the curve's optimal point it rises gently; above it, a steep second slope kicks in to pull the pool back into balance.

Why is the yield I earn lower than what borrowers pay?

Because only the borrowed part of the pool earns interest, and the protocol keeps a cut called the reserve factor. Your deposit yield is roughly the borrow rate multiplied by utilization and by one minus the reserve factor — so at 80% utilization you already receive well under the borrow rate, before fees. It's the single most common surprise for new lenders.

Why did my lending rate suddenly spike?

Because utilization crossed the curve's "kink." Past that optimal point, protocols raise rates steeply to attract deposits and pressure borrowers to repay. A sudden spike almost always means borrowing surged relative to supply — which is also the moment your ability to withdraw is most constrained.

Where can I actually check utilization and rates?

On DeFiLlama, each protocol's own market screen, or a block explorer like Etherscan for the raw on-chain values — no paid dashboard required. Look at Aave and Compound as well as newer markets like Morpho, Spark, and Sky. Rates move constantly and vary by chain and stablecoin, so read them live rather than trusting a static number.

Where did the high CeFi yields (BlockFi, Celsius) come from?

From undisclosed risk. Those platforms took deposits and lent or invested them opaquely, with no on-chain pool to inspect, then failed when the bets went wrong — both filed for bankruptcy in 2022, followed by SEC and FTC action. If you can't trace a yield to a transparent mechanism, treat the yield itself as the red flag.

Author's Insight

After years of lending stablecoins across these markets, the habit that has protected me most is boringly simple: I look at utilization before I look at the yield. Early on I did it backwards, chasing the highest advertised rate, and I learned the hard way that the best-looking number is often attached to the pool you'll most regret being stuck in. The rate is downstream; utilization is the cause. Once I started reading the cause instead of the symptom, the whole market got quieter and easier to navigate — and I stopped mistaking a risk premium for a bargain. The protocols that survive show you their formula; the ones that blow up ask you to trust a promise. I lend where I can read the math.

Bottom Line

A stablecoin lending rate is not a quote, it's the output of a utilization curve you can read in advance. High yields signal heavy utilization, which means thinner liquidity and a harder exit, not a smarter trade. The transparent, on-chain version of this market lets you verify where your yield comes from and whether you can withdraw; the opaque, centralized version — the one that promised fixed high returns and collapsed — did not. Check utilization before rate, trace the yield to real demand, size for the moments you can't exit, and never lend into a number you can't see the mechanism behind.