Every yield in DeFi is paid by someone. The single most useful habit an investor can build is asking a blunt question before depositing a dollar: who is paying this, and why? If the answer is "other users, through fees," the yield is real and can last. If the answer is "the protocol, by printing its own token," the yield is a countdown timer. This guide traces DeFi yield back to its actual sources, gives you a test for whether a return is sustainable, and explains the shift that has quietly redefined "real yield" in 2026 — the arrival of off-chain interest through tokenized real-world assets.

What "Real Yield" Means

The phrase "real yield" entered the DeFi vocabulary after the 2021–2022 farming bubble collapsed. During the boom, protocols advertised four-figure APYs paid almost entirely in their own freshly minted governance tokens. When the inflow of new buyers slowed, those tokens cratered, and the "yield" turned out to be a wealth transfer from late depositors to early ones.

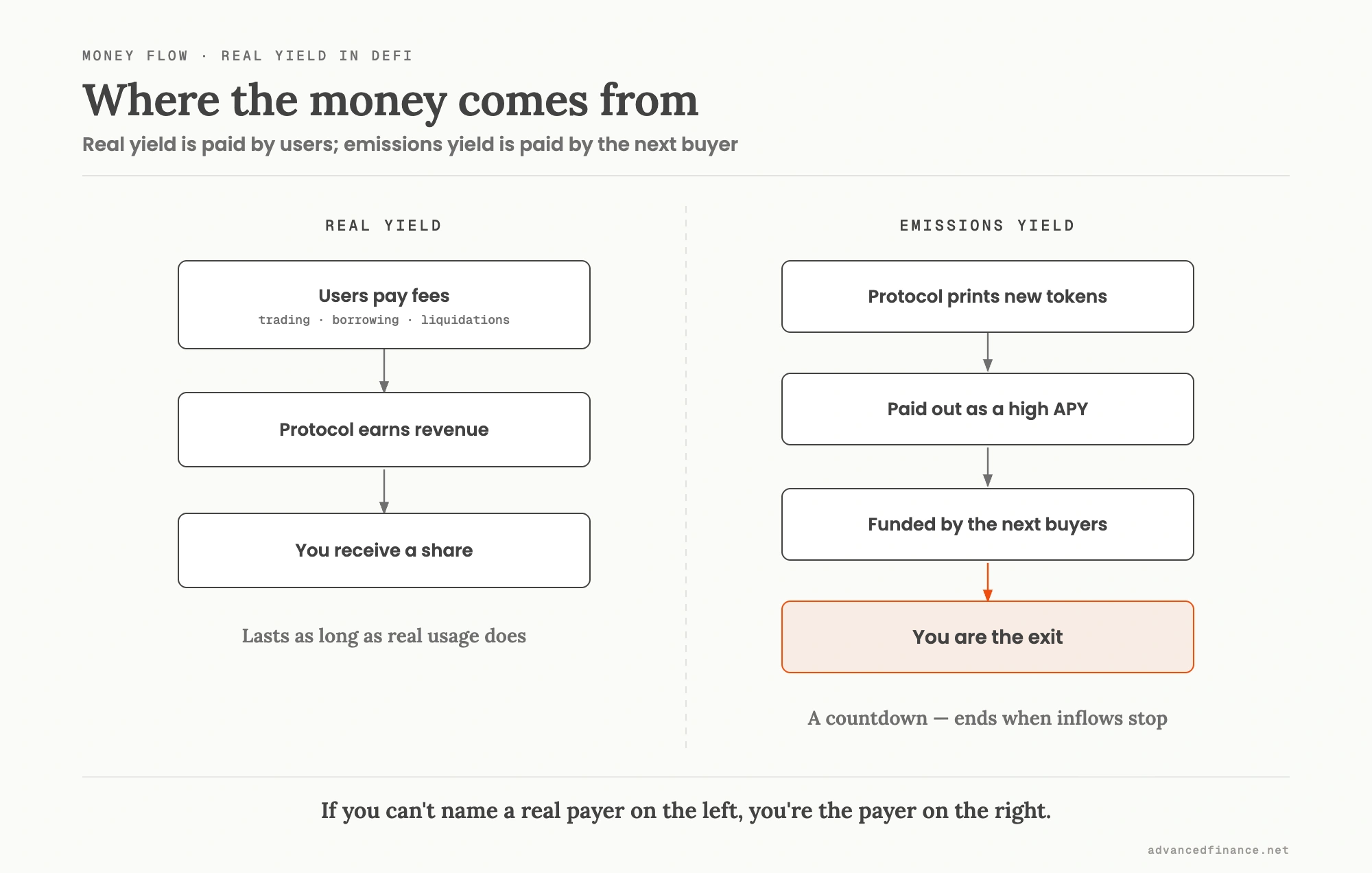

Real yield is the opposite: income distributed from genuine protocol revenue — the fees, spreads, and penalties that outside users actually pay — rather than from token inflation. The distinction is now measurable, and it is trending the right way. Industry data shows the share of protocol revenue passed through to token holders roughly tripled during 2025, from a historical average near 5% to over 15%. DeFi has slowly grown up: more of the yield now comes from a business, not a printing press.

The Five Sources of Yield

Almost every DeFi return traces back to one of five buckets. Four are real; one only looks real.

| Source | What it is | Real? |

|---|---|---|

| Fees & spreads | DEX trading fees, the lending interest spread, perpetual-swap funding | Real — paid by users |

| Liquidations | Penalties collected when over-leveraged borrowers are closed out | Real, but lumpy |

| Staking issuance | New tokens minted to pay validators for securing a proof-of-stake chain | Real but dilutive |

| Off-chain interest (RWA) | Yield from tokenized Treasuries and credit, earned outside the chain | Real but imported |

| Token emissions | Governance or "farm" tokens printed to attract deposits | Not real — a transfer |

Five sources of DeFi yield and whether each is real revenue or a temporary subsidy.

Fees are the gold standard because they scale with genuine usage: when people trade on a DEX or borrow on a lending market, a slice of what they pay flows to liquidity providers and token holders. On a DEX charging a 0.05% swap fee, for example, every $10,000 traded generates $5 in fees, split between the liquidity providers who supplied the pool and, on many protocols, the token holders who govern it — a small cut of a real transaction, not a printed reward. Lending yield in particular is just the spread between what borrowers pay and what depositors receive, which is why it moves with supply and demand for stablecoin credit. Staking issuance is real in that it compensates you for a real service (securing the network), but it is paid in new supply, so your token count rises while everyone's slice is diluted — a subtler cost than farm-token inflation, but a cost. Emissions are the odd one out: printing a token and handing it to depositors creates no value, it only redistributes it.

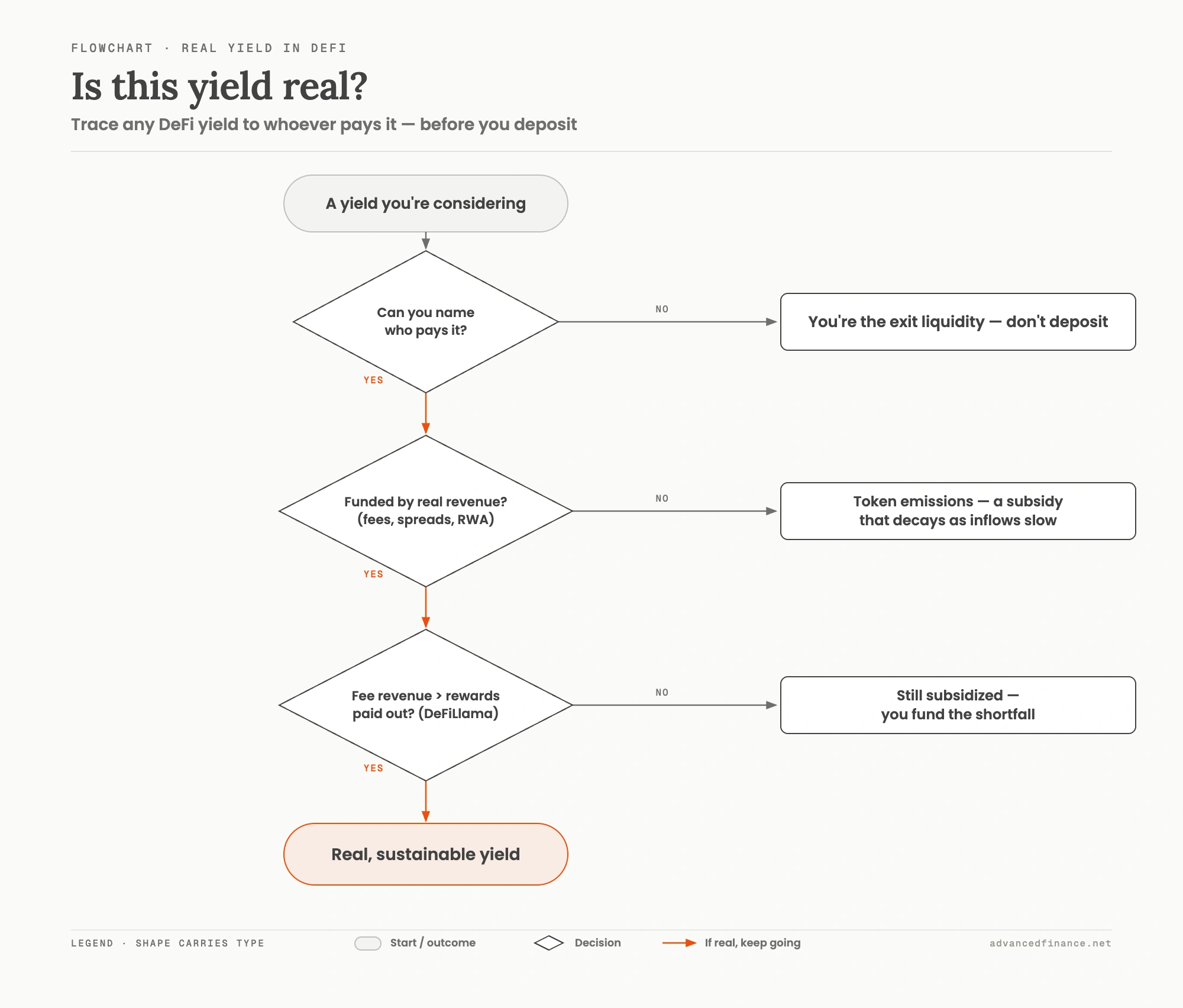

The Sustainability Test

There is a single question that separates a durable yield from a decaying one: does the protocol earn more in real fees than it pays out in incentives?

If a protocol collects $1 million a month in fees and emits $5 million in token rewards to prop up its APY, the advertised yield is 80% subsidy. That gap has to close — either the token price falls, the emissions get cut, or both — and the people still farming when it closes are the ones who fund the exit. You do not have to guess at these numbers. Public dashboards like DeFiLlama's protocol-revenue rankings show what each protocol actually earns, so you can compare real revenue against the rewards being paid. The test in one line: if you cannot point to the fee stream that funds your yield, assume the emissions are the yield, and that you are the exit liquidity.

The encouraging news is that a handful of protocols now pass this test emphatically. At its 2025 peak, the perpetuals exchange Hyperliquid distributed over $74 million to token holders in a single month — not printed tokens, but a share of real trading fees. That is what a mature "real yield" business looks like.

It helps to see how a few well-known protocols actually fund their payouts. The mechanic matters more than the headline rate; for live fee and revenue figures, cross-check each name on DeFiLlama.

| Protocol | What it is | Where the yield comes from | Verdict |

|---|---|---|---|

| Aave | Lending market | Interest paid by borrowers (the deposit-to-borrow spread) | Real |

| GMX | Perp & spot DEX | Trading and borrow fees, shared with liquidity providers and stakers in blue-chip assets | Real |

| Hyperliquid | Perp DEX | Trading fees, distributed to stakers and used for buybacks | Real |

| Curve | Stablecoin DEX | Trading fees to veCRV lockers, plus CRV token emissions to LPs | Mixed (fees + emissions) |

| Tokenized Treasuries | RWA funds (e.g. Ondo, BlackRock's BUIDL) | US Treasury interest earned off-chain | Real but imported |

Named DeFi protocols and where their yield actually comes from.

The 2026 Shift to RWAs

The biggest change to DeFi yield in 2026 is that a lot of it no longer comes from DeFi at all. Real-world assets — chiefly tokenized US Treasuries and private credit — have grown into one of the largest categories on-chain, climbing past $17 billion in value from roughly $12 billion in late 2024 to become the fifth-largest DeFi sector. You can watch the sector in near-real time on DeFiLlama's RWA dashboard.

Here is the framing that matters: RWA yield is real, but it is imported. When a tokenized Treasury fund pays you, that yield is simply whatever short-term US government debt is paying, wrapped in a smart contract. You are not earning a DeFi-native return; you are earning the Treasury rate, minus a fee, plus smart-contract and custody risk. For a lot of investors that is a genuinely good deal — a familiar, government-backed yield with on-chain liquidity. But call it what it is. If the off-chain rate falls, so does your "DeFi" yield, because the two were always the same number.

How to Trace a Yield

Before depositing, run any opportunity through four quick checks:

- Name the payer. Say out loud who funds the return — traders, borrowers, the US Treasury, or new token buyers. If you cannot, stop here.

- Split real from printed. Check the protocol's fee revenue against its emissions on a dashboard like DeFiLlama's yield rankings. A high APY next to near-zero fee revenue is a subsidy, not a business.

- Compare to the risk-free rate. If a "safe" stablecoin strategy pays far above what tokenized Treasuries yield, the excess is compensation for a risk you have not identified yet.

- Check the audits and the lockups. Real yield trapped behind an unaudited contract or a long withdrawal queue can still go to zero. The same due diligence you would use to spot a scam or rug pull applies to any yield source.

Common Traps

- APY blindness. A 400% APY paid in a token that falls 90% is a deeply negative real return. Always denominate the yield in a stable unit, not in the farm token.

- Mercenary emissions. Rewards designed to attract "mercenary capital" evaporate the moment a better farm appears, taking the token price with them. High emissions attract the least loyal money.

- Recursive leverage. Looping a staked asset to borrow and re-stake can turn a 3% yield into a headline number, but a small price move can trigger a liquidation that wipes the principal. This is the same loan-to-value risk that governs any collateralized position.

- Impermanent loss. Much liquidity-pool yield is quietly offset by impermanent loss: when the two assets in a pool diverge in price, the pool rebalances against you, and the fees you collected can be smaller than the loss. A pool's advertised APR is not the same as what you keep — on volatile pairs the gap can be brutal.

- Confusing staking rewards with free money. Base staking on Ethereum pays around 3% today, and that is real — but it is issuance, and it competes directly with the far simpler decision to just hold. Weigh it against staking versus yield farming before chasing a few extra points.

FAQ

What is the difference between real yield and token emissions?

Real yield is your share of income the protocol actually earns — trading fees, the lending spread, liquidation penalties. Token emissions are freshly printed governance or farm tokens handed to depositors. Emissions create no value; they redistribute it from later buyers to earlier ones, which is why an emissions-funded APY collapses once new deposits slow.

Which protocols actually pay real yield?

Fee-funded protocols like Aave (the lending spread), GMX and Hyperliquid (trading fees), and tokenized-Treasury funds (off-chain interest) pay from genuine revenue. Others, like Curve, mix real fees with heavy token emissions. Rather than trust any list, check each protocol's fee revenue against its rewards on a dashboard like DeFiLlama before depositing.

Doesn't liquidity-pool yield come with impermanent loss?

Yes, and it is often overlooked. When you supply two assets to a pool and their prices diverge, the pool rebalances against you, so the fee yield you earn can be smaller than the impermanent loss. A pool's advertised APR is a gross number — subtract impermanent loss to see what you actually keep, especially on volatile pairs.

What is the difference between APR and APY?

APR is the simple annual rate; APY assumes those returns are compounded over the year, which inflates the headline figure. Farm dashboards usually quote APY, often assuming frequent compounding of a reward token whose price may fall faster than it compounds. Convert everything to a stable-denominated number before comparing.

Is RWA yield real, and will it last?

It is real but imported: a tokenized Treasury pays you the underlying government-bond rate wrapped in a smart contract. It lasts as long as those off-chain rates do — if short-term Treasury yields fall, your "DeFi" RWA yield falls with them, because they were always the same number minus a fee.

Author's Insight

After years of watching DeFi cycles, the single filter that has protected me most is refusing to deposit into anything whose yield I cannot explain in one sentence. "I earn a share of the trading fees" is a sentence. "The APY is 320%" is not an explanation, it is a number. Every blow-up I have watched from the sidelines shared the same tell: a yield nobody could source, propped up by a token everyone planned to sell to someone else. The boring yields — fees, spreads, Treasury rates — are boring precisely because they are real, and they are the ones still standing after each cycle clears.

Bottom Line

Real yield is not a marketing label; it is a question you answer before you deposit. Trace the return to fees, spreads, liquidations, or off-chain interest and it can last; trace it to token emissions and it is a countdown. In 2026 the largest pool of "real yield" is increasingly imported through tokenized Treasuries — genuinely useful, but just the off-chain rate in an on-chain wrapper. Check real revenue against emissions on a public dashboard, denominate every APY in a stable unit, and if you cannot name who is paying you, assume it is you. The yields you can explain are the ones you get to keep.