Almost every explainer opens the same way: decentralized finance replaces banks by cutting out the middleman. That is half true, and the missing half is the one that matters. DeFi does re-create nearly everything a bank does — holding money, lending it, exchanging it, moving it — in open-source code anyone can use without asking permission. What it does not re-create is the thick layer of protection a bank wraps around those functions: insured deposits, reversible payments, a human to call when something goes wrong, and a central bank standing behind the entire system. Remove the intermediary and you remove that safety net with it. This guide goes function by function through what DeFi actually replaces, how each replacement works, and — the part most guides skip — which protection you give up and who then carries the risk. The short answer to that last question is: you.

DeFi in Plain Terms

If you are new to this, start here. Decentralized finance is a set of financial services — lending, trading, saving, payments — that run as open-source programs on a public blockchain instead of inside a company. Those programs are called smart contracts: self-executing code that holds funds and follows fixed, public rules no employee can override. You interact through a wallet, which is not an account at an institution but a pair of cryptographic keys; whoever holds the keys controls the money. That single design choice — rules in public code, control by private key — is what removes the intermediary. It is also what removes the intermediary’s protections, which is the thread running through everything below.

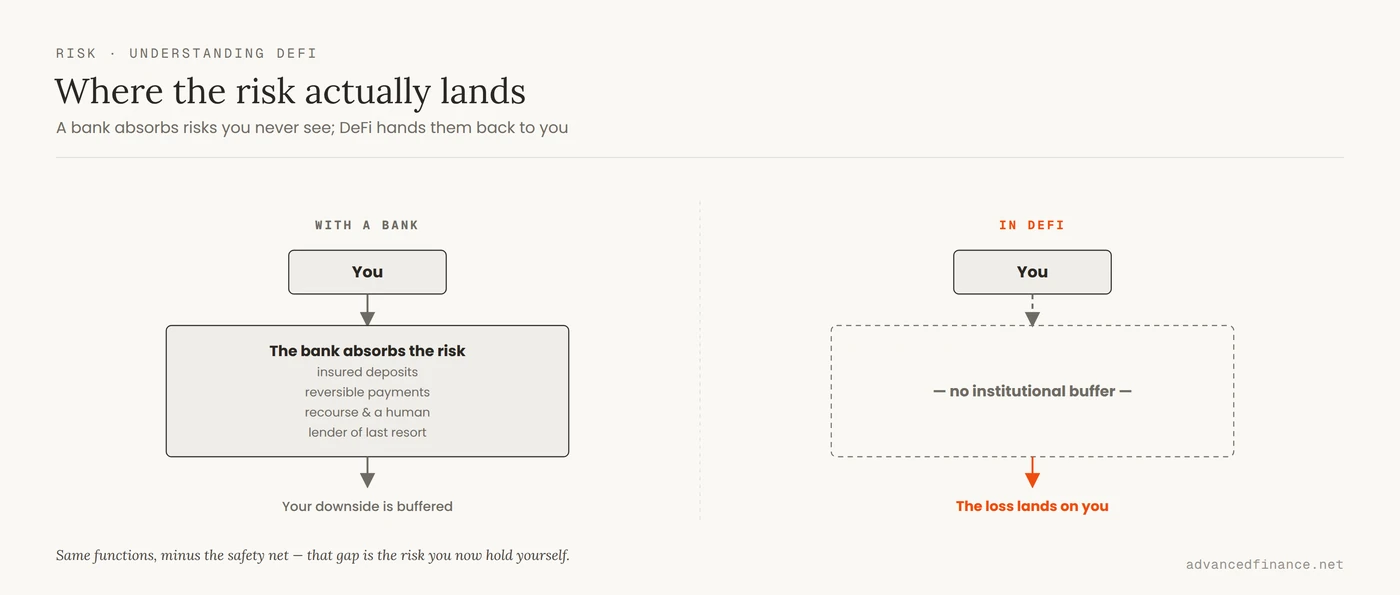

What a Bank Really Provides

It helps to separate two things a bank sells you as one product. The first is a set of functions: a place to store money, credit when you need it, a way to exchange currencies, and rails to send payments. The second is a set of protections you rarely think about until they matter — deposit insurance, the ability to reverse a fraudulent charge, someone accountable for mistakes, and a lender of last resort that can inject emergency liquidity when confidence cracks. In the United States that insurance is concrete: the FDIC guarantees deposits up to $250,000 per depositor, per bank, per ownership category.

DeFi unbundles these. It re-implements the functions brilliantly and drops the protections entirely. The Bank for International Settlements made the point plainly, warning that DeFi lacks the shock absorbers, such as banks, that can provide emergency liquidity in a crisis — and that the promise of full decentralization is partly a “decentralisation illusion.” Here is the whole article in one view: each function a bank performs, how DeFi rebuilds it, and the protection that does not come along.

| Function | What a bank provides | DeFi mechanism | Protection removed |

|---|---|---|---|

| Deposits & payments | Insured balances, reversible transfers | Wallets, stablecoin transfers | Deposit insurance, chargebacks |

| Lending | Underwriting, forbearance | Over-collateralized smart-contract loans | Human judgment, recourse, workout |

| Trading | Market makers obligated to quote | Automated market makers (pools) | Fair-market obligation; you bear the loss |

| Custody | Safekeeping, account recovery | Self-custody via private keys | Recovery, fraud reversal, insurance |

| Systemic backstop | Lender of last resort, insurance | Over-collateralization only | Emergency liquidity, bailout |

What DeFi Replaces

Take a bank’s core jobs one at a time. Each has a DeFi replacement — and each replacement quietly drops a protection you were relying on.

Lending without a loan officer

A bank loan runs through a credit officer who judges whether you will repay. Protocols such as Aave, Compound, and MakerDAO replace that judgment with collateral and code. You do not fill in an application or reveal your income; you deposit crypto worth more than you borrow, and a smart contract lends against it automatically. The interest rate is not set by an officer either — it is the output of a supply-and-demand curve that reprices continuously. Because there is no one to assess your creditworthiness, the system demands you over-collateralize — often depositing $150 or more to borrow $100 — and it enforces repayment not with a phone call but with an automatic sale.

That is the trade. There is no forbearance, no restructuring, no human to negotiate with when the market turns against you; if your collateral falls far enough, the contract liquidates it in seconds. It is worth understanding exactly how the loan-to-value ratio and liquidation threshold govern a crypto-backed loan before you ever open one, because the machine will not give you the benefit of the doubt.

Markets without a market maker

On a traditional exchange, professional market makers quote prices and stand ready to trade. DeFi replaces them with an automated market maker: a pool of two assets whose price is set by a formula rather than a person. Uniswap popularized the constant-product model, where the product of the two reserves stays fixed and every trade moves the price along that curve. Anyone can supply the pool and earn a share of the trading fees — the market maker’s role, opened to the public.

What disappears is any obligation to make a fair market. No one is required to quote, spreads can gap in a fast move, and the people supplying liquidity absorb the losses a professional desk would hedge. That last cost has a name: impermanent loss. Supply an ETH/stablecoin pool and let ETH double in price, and the formula automatically sells your ETH into the rise — you end up with about 5.7% less value than if you had simply held the two assets. If you plan to be that liquidity provider, treat it as a real position, and know the difference between staking and yield farming before you commit capital.

When custody becomes your job

A bank is a custodian: it holds your money and is accountable for keeping it. In DeFi, custody is your job. Your funds live at an address controlled by a private key, and whoever holds that key holds the money. There is no branch, no account recovery, no fraud department. Lose the key and the funds are gone; sign a malicious transaction and they are gone just as fast, with no chargeback to undo it.

This is genuine self-sovereignty and genuine exposure at the same time. A hardware wallet, careful transaction hygiene, and a healthy suspicion of anything that asks you to connect and approve are not optional extras — they are the safety net you now build yourself. A large share of losses in this space are not protocol failures at all but ordinary theft, so learning to spot scams and rug pulls before you invest does more for your safety than any single security tool.

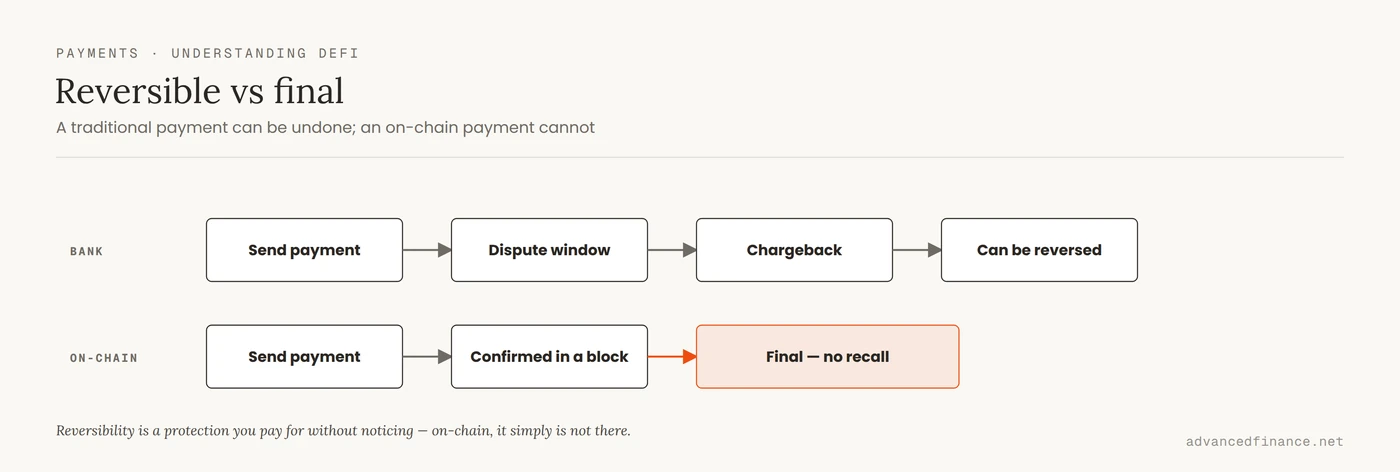

Payments that can't be recalled

This is where DeFi is most obviously better — and most quietly dangerous. Sending value on-chain settles in seconds for a few cents, against a global average remittance cost the World Bank still puts at 6.36% of the amount sent. For anyone moving money across borders, that gap is life-changing. Stablecoins are the workhorse here, and it helps to understand how stablecoins bridge fiat and crypto before you rely on them.

But the same property that makes on-chain payment fast makes it unforgiving: it is final. There is no chargeback, no dispute window, no bank to claw a payment back from a scammer or reverse a mistyped address. In traditional payments, reversibility is a feature you are paying for without noticing. On-chain, you are not paying for it because it does not exist.

No lender of last resort

Every function above removes a local protection. This one removes the systemic one. When a bank runs into trouble, a central bank can step in as lender of last resort; when depositors panic, insurance caps the damage. DeFi has neither. Over-collateralization protects a single loan, but nothing protects the system when confidence evaporates at once.

We have seen what that looks like. The algorithmic stablecoin TerraUSD collapsed in May 2022, wiping out tens of billions in days with no backstop to arrest the spiral. Even a reputable, fully-reserved stablecoin, USDC, briefly slipped to about $0.87 in March 2023 when one of its banking partners failed — it recovered, but only because a traditional bank rescue happened off-chain. The BIS flagged exactly this fragility: liquidity mismatch and run risk with no institutional shock absorber. A high advertised yield does not change that math, which is why it pays to insist on yields that come from real protocol revenue rather than token emissions that vanish the moment inflows slow.

Where DeFi Genuinely Wins

None of this makes DeFi a gimmick. Its advantages are real and, in some cases, decisive. It is permissionless: the World Bank’s latest Global Findex shows 79% of adults now have an account, which still leaves roughly one in five without one — and a wallet asks no one’s permission. It is transparent: balances and code are public and auditable, not hidden on a private ledger. It is composable, so services snap together like building blocks. And it runs continuously, settling in seconds at a fraction of legacy cost. Much of the practical progress on fees and speed is happening on cheaper networks, which is why it is worth knowing where value accrues across Layer 1 and Layer 2.

Using DeFi Without Getting Hurt

The honest way to use DeFi is to take its functions and supply your own version of the protections it strips out. Favor established, heavily-audited protocols over whatever is advertising the highest number this week. Check who can change the rules, too: many protocols keep admin keys or upgradeable contracts that let a team — or an attacker who compromises them — rewrite the code you trusted, so prefer governance that is time-locked or multisig-controlled. Assume every payment and signature is final, hold the bulk of your assets in a hardware wallet, and size positions so a failure or a liquidation is survivable, not ruinous.

It helps to see where the protections drop out in a single sequence. A simple borrow looks like this:

- Move cash to a wallet. The moment funds leave your bank, deposit insurance and chargebacks stop applying.

- Buy a stablecoin. Value now settles on-chain — fast and final, with no dispute window.

- Supply it to a lending protocol. A smart contract, not a banker, now holds and lends your collateral.

- Borrow against it. You over-collateralize; a price drop can trigger automatic liquidation with no call and no grace period.

- Repay to unlock your collateral. Miss the window and the code, not a person, decides what happens next.

Every step buys efficiency and hands you a risk the bank used to hold. Treat any yield as a claim to verify, not a gift — if you cannot name who pays it, you are probably the one paying — and DeFi becomes a powerful complement to the banking system rather than a reckless replacement for it.

FAQ

Is DeFi safe if I stick to big protocols?

Using large, long-audited protocols lowers your smart-contract risk, and that is worth doing. But it does not add insurance, reversibility, or a backstop — those simply do not exist in DeFi regardless of the protocol’s size. “Blue-chip” reduces one category of risk, not all of them.

If a stablecoin depegs, can I get my money back?

There is no guarantee. A fully-reserved stablecoin may recover if its issuer can redeem reserves, but that is a promise from the issuer, not deposit insurance. An algorithmic stablecoin can fail outright, as TerraUSD did. Nothing on-chain reimburses you.

Do I need to give up my bank to use DeFi?

No, and you probably should not. The sensible model is complementary: keep insured deposits and reversible payments where they belong, and use DeFi for the specific things it does better, such as low-cost transfers or transparent, revenue-backed yield.

What happens if I send crypto to the wrong address?

In almost every case it is gone. On-chain transfers are final and there is no institution that can reverse them. This is why verifying the address and sending a small test amount first are basic discipline, not paranoia.

Is DeFi yield just free money?

No. Sustainable yield is paid out of real fees, spreads, or lending demand; unsustainable yield is paid out of freshly-printed tokens and lasts only while new money arrives. Learning to tell the two apart is the single most valuable habit in the space.

Author's Insight

After years of using these protocols with my own money, the mental shift that helped me most was to stop asking whether DeFi is “better” than banking and start asking what each tool actually removes. A bank charges you spread and friction, and in exchange it absorbs a set of risks you never see. DeFi hands those risks back to you along with the keys. That is a fair trade for some jobs — moving money cheaply, earning transparent yield — and a bad one for others, like parking your emergency savings. I keep insured cash in a bank precisely so I can afford to take deliberate, sized risks on-chain. The people who get hurt are almost never the ones who understood the trade-off; they are the ones who were told there wasn’t one.

Bottom Line

DeFi does not so much replace banks as rebuild their functions without the safety net that made those functions feel safe. Lending, market-making, custody, and payments all work without intermediaries — and without insurance, reversibility, recourse, or a lender of last resort. The efficiency is real, and so is the risk transfer. Use DeFi for what it does better, supply your own protections where it strips them out, and never mistake the absence of a middleman for the absence of risk.