This comprehensive guide explores the reality of AI trading bots, moving beyond the hype to uncover how they actually operate in live markets. It breaks down the critical differences between retail and institutional (prop desk) infrastructure, details the essential tech stack from data ingestion to execution, and explains why rigorous risk management and a reliable "kill switch" are far more important than the predictive model itself.

What AI Bots Really Do

AI trading bots do not replace trading judgment. They compress it.

A bot takes market data, transforms it into signals, applies rules, sizes positions, sends orders, and monitors whether the system is still behaving inside acceptable boundaries. The AI layer may classify news, detect market regimes, forecast short-term volatility, rank setups, or decide when not to trade. But the profitable part is rarely the model alone. The edge usually lives in the connection between signal quality, execution, risk control, and market structure.

When I first deployed a live bot, I expected the model to be the difficult part. It was not. The model was trained, tested, and documented. The problems started when the exchange API returned delayed fills, the bot saw stale prices, and the risk engine interpreted partial execution as open exposure. That was my first real lesson: backtests fail politely, live systems fail loudly.

The hype around AI trading usually skips this. A clean equity curve in a notebook is not a trading system. It is a research artifact. A trading system has to survive bad data, rejected orders, network delays, exchange maintenance, duplicate signals, funding spikes, position drift, and days when the model is simply wrong.

The May 2023 fake Pentagon explosion image is a better warning than the usual recycled Knight Capital story. A fabricated image, widely described as AI-generated or apparently AI-generated, spread online and briefly shook U.S. markets. The point for traders is not just that fake news exists. The point is that machine-generated content can enter machine-readable information channels before humans validate it. That is the real AI-vs-AI market risk: synthetic information can trigger automated reaction before truth catches up.

Retail Build Path

Retail algo trading is not miniature hedge fund trading. The budget, execution quality, data access, and operational risk are completely different.

For a trader with under $50k in deployable capital, the realistic stack is usually Python, a broker API such as Alpaca, a platform such as QuantConnect, MT5 for FX/CFDs where available, or a crypto exchange API. The bot may run on a home server, a VPS, or a small cloud instance. This is enough to build, test, and run basic systems, but it is not enough to compete in speed-sensitive strategies.

The mistake I see most often in production is retail traders choosing strategies that require institutional infrastructure. If your idea depends on reacting faster than professional market makers, you are probably not the competitor. You are the liquidity. HFT firms have better feeds, lower latency, exchange relationships, and co-located servers. A retail trader cannot fix that with a Python package.

Retail bots should focus on slower edges: swing signals, portfolio rebalancing, volatility filters, mean reversion on liquid crypto pairs, risk-based position sizing, or systematic setup detection. A good place to start is not "predict the next candle," but "define the setup precisely enough that a machine can reject most bad trades." That is where structured signal work, such as identifying repeatable trade conditions, becomes useful. See this discussion of high-probability trade setups when designing the signal layer.

Retail traders also need to be honest about costs. Commissions, spreads, slippage, borrow fees, funding rates, and taxes can destroy strategies that look profitable in a frictionless backtest. Most retail algo traders lose money because they underestimate execution costs, overfit to historical data, and stop monitoring the bot once it goes live.

Prop Desk Build Path

Institutional and prop trading systems are a different species.

A prop desk may use co-location, direct market access, FIX gateways, dedicated data lines, internal risk servers, and separate environments for research, simulation, staging, and production. The trading model is only one service inside a larger system. Order routing, risk checks, compliance logs, monitoring, and reconciliation often matter more than the prediction layer.

At this level, infrastructure defines what strategies are possible. If the desk is running intraday equities, latency and queue position may be central. If the desk is trading futures spreads, stable connectivity and exchange-grade risk controls matter. If the desk is running cross-exchange crypto arbitrage, the challenge is less "AI" and more inventory management, withdrawal delays, exchange outages, and fragmented liquidity.

The institutional advantage is not just capital. It is feedback speed. A desk can measure slippage by venue, model fill probability, compare live fills to simulated fills, and retire strategies as edge decays. Retail traders often notice decay only after the equity curve has already rolled over.

This is why I separate research edge from production edge. Research edge asks: "Did this signal work historically?" Production edge asks: "Can we capture it after fees, latency, risk limits, and competitors?" The second question is where many AI systems die.

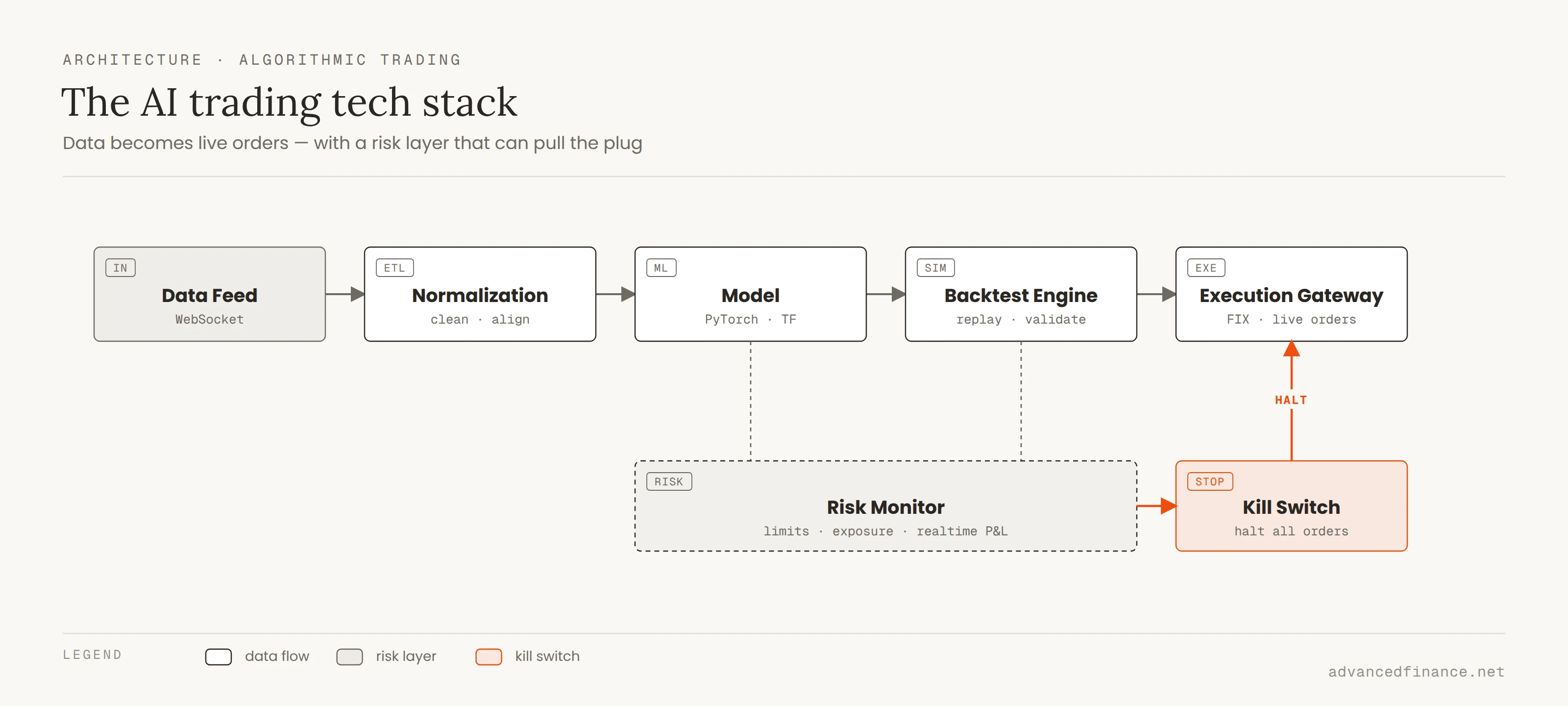

Tech Stack Map

A practical AI trading bot can be visualized as a pipeline:

- Data Feed (WebSocket): This is the live market input: prices, order book updates, trades, funding rates, or news. For alternative data, the hard part is not collecting more information; it is proving that the data arrives early enough and cleanly enough to trade. For a broader view, see how big data is changing financial market research.

- Normalization Layer: Raw exchange and broker data is messy. This layer standardizes timestamps, symbols, decimal precision, missing values, and event ordering so the model is not trained on one format and traded on another.

- Model (PyTorch / TF): The model converts normalized inputs into probabilities, classifications, rankings, or signals. It may score sentiment, classify volatility regimes, detect anomalies, or estimate expected return.

- Backtest Engine: Tools such as Backtrader or Zipline simulate how the strategy would have traded historically. A serious backtest must include fees, slippage, realistic fills, latency assumptions, and position limits.

- Execution Gateway: This is where signals become orders. REST APIs are common for retail systems, while FIX is standard in more professional environments where speed, session control, and order-state management matter.

- Risk Monitor + Kill Switch: This watches exposure, drawdown, order frequency, rejected orders, stale data, and model behavior. It should be able to flatten positions or stop trading without asking the model for permission.

A simple sentiment signal might look like this:

import requests

from execution import send_order

from risk import position_size, kill_switch_clear

headline = requests.get(NEWS_API_URL, timeout=2).json()["headline"]

score = sentiment_model.score(headline) # returns -1.0 to +1.0

if score > 0.65 and market_is_liquid("ETHUSDT"):

side = "BUY"

elif score < -0.65 and market_is_liquid("ETHUSDT"):

side = "SELL"

else:

side = None

if side and kill_switch_clear():

qty = position_size(symbol="ETHUSDT", risk_pct=0.01)

send_order(symbol="ETHUSDT", side=side, quantity=qty)

This is not a full trading script. It is the logic flow: fetch information, score it, convert it into a trade decision, size the position, then check risk before execution.

Latency And Execution

Latency does not matter equally for every strategy. A weekly ETF rotation model can tolerate slow execution. A market-making bot cannot.

| Connection Type | Typical Latency | Best For |

|---|---|---|

| REST API | 50-200ms | Swing/position bots |

| WebSocket | 5-20ms | Intraday crypto bots |

| FIX Protocol | 1-5ms | Equities, institutional |

| Co-location | <1ms | HFT only |

These ranges are practical engineering estimates, not promises. Actual latency depends on venue, broker, order type, hosting location, network path, and how you measure round-trip time. The important point is not whether your REST call is 80ms or 180ms. The important point is whether the strategy still has edge after the delay.

The structural issue for retail traders is simple: if a strategy's edge disappears when execution is 100 milliseconds slower, it is probably not a retail strategy. The trader with a VPS and REST API should not be competing against firms that rent rack space near exchange matching engines.

Execution quality also changes the meaning of a backtest. A model with a 58% win rate can lose money if winners are small and slippage expands during exits. A model with a 42% win rate can make money if average winners are much larger than average losers. That is why win rate alone is one of the most misleading metrics in system evaluation. This is covered in more detail in win rate versus risk-reward.

A Testable Strategy

Here is a more useful case study than a generic "hedge fund uses AI" paragraph: a mean-reversion strategy on ETH/USDT on Binance.

The logic is intentionally simple. Calculate the 20-period moving average and standard deviation of ETH/USDT. When price moves more than two standard deviations below the 20-period mean, enter long. When price moves more than two standard deviations above the mean, enter short or avoid longs, depending on whether shorting is allowed. Exit when price returns to the mean. Add a volatility filter so the bot avoids trading during extreme news events or thin liquidity.

The reason this example matters is that it can be tested. It has a defined market, entry rule, exit rule, lookback window, and risk model. There is no vague claim about "AI finding hidden patterns." You can run it, break it, and compare live results to the backtest.

A sample 12-month backtest summary for this kind of strategy might look like this:

| Metric | Example Result |

|---|---|

| Market | ETH/USDT on Binance |

| Lookback | 20 periods |

| Entry | >2 standard deviations from mean |

| Exit | Return to 20-period mean |

| Sharpe Ratio | ~1.2 |

| Max Drawdown | ~15% |

| Win Rate | ~58% |

| Test Window | 12 months |

Do not publish numbers like these as audited performance unless they come from your own exportable backtest report, including timestamps, fees, slippage assumptions, and raw trade logs. The value of the table is that it shows what a serious strategy review should contain. If all you have is "the bot wins 58% of trades," you do not have enough information to judge the system.

The same strategy can also produce a dangerous result that looks attractive at first glance. Here is an example of a backtest profile that looks good by win rate but destroys the account through drawdowns: a 63% win rate, Sharpe Ratio of -1.2, max drawdown above 35%, and repeated large losses during trending conditions. That is the kind of system newer algo traders often keep because it "wins most of the time." In reality, the loss distribution is doing the damage.

Mean reversion can look excellent in choppy markets and terrible in trending markets. If ETH enters a strong directional move, the bot may repeatedly fade the trend and compound losses.

This is where many traders misunderstand edge. A strategy can have worked and then stop working. The market adapts, competitors crowd the trade, fees change, liquidity shifts, or volatility moves into a different regime. For a deeper framework, read where trading profits actually come from.

Where Bots Fail

After running bots 24/7 for months, the real enemy is not one catastrophic bug. It is small mismatches between the model's assumptions and live market behavior.

Backtests assume data is clean. Live feeds drop packets. Backtests assume candles close once. Live systems may receive revised bars or duplicate events. Backtests assume orders fill at modeled prices. Live orders get partial fills, rejected orders, stale quotes, and slippage exactly when risk is highest.

Overfitting is the classic failure. A trader optimizes dozens of parameters until the equity curve looks smooth, then discovers the model memorized historical noise. The warning signs are easy to recognize: too many parameters, performance concentrated in a few trades, unstable results across time periods, and strategy logic that cannot be explained without pointing to the optimizer.

The other failure is risk blindness. A bot that sizes every trade the same way treats calm markets and panic markets as equal. They are not equal. Volatility-adjusted sizing, max daily loss limits, exposure caps, and automatic shutdown rules are not optional. They are the difference between a bad day and an account-ending event. This is why every automated system needs explicit risk management and position sizing.

Most retail bots do not fail because the developer is stupid. They fail because the developer builds a research tool and mistakes it for production infrastructure.

FAQ

How do I detect overfitting?

Start by separating development, validation, and untouched out-of-sample data. Then run walk-forward tests, parameter sensitivity checks, and market-regime splits. If small parameter changes destroy performance, the strategy is probably fitted to noise rather than exploiting a durable edge.

Why does live performance lag?

Live performance usually lags because the backtest underestimates friction. Slippage, spreads, rejected orders, latency, partial fills, and exchange downtime all reduce captured edge. The gap is largest when the strategy trades frequently or depends on precise entry and exit prices.

Is crypto data worse than equities?

Crypto data is easier to access but often harder to trust. Exchange APIs vary in quality, symbols are inconsistent, outages are common, and historical order book data can be expensive or incomplete. Equities data is more standardized, but professional-grade feeds cost more because they must handle corporate actions such as splits, dividends, symbol changes, delistings, and adjusted historical prices.

What rules apply in the US?

Running a bot on U.S. exchanges can involve broker rules, exchange rules, pattern day trading constraints, market manipulation rules, and, for advisers or pooled capital, registration or exemption questions. A personal bot trading your own account is different from managing money for others. Anyone deploying capital professionally should consult a qualified regulatory attorney before launch.

What is the minimum 24/7 setup?

At minimum, use a reliable VPS or cloud server, process monitoring, restart logic, encrypted API keys, logging, alerts, database backups, and a manual override. The bot should detect stale data, rejected orders, position mismatch, and excessive drawdown. A system that cannot wake you up when it breaks is not ready to trade unattended.

Author's Insight

The most valuable part of an AI trading bot is not the entry signal. It is the exit logic and the kill switch. Entries get attention because they feel intelligent. Exits determine whether the system survives. Every bot I trust has predefined exits, max loss rules, stale-data checks, order rejection limits, and a hard stop that can disable trading when the environment no longer matches the model's assumptions.

My rule is simple: the model can suggest trades, but the risk layer has veto power. If volatility spikes, data goes stale, drawdown breaches limits, or execution quality deteriorates, the bot should stop first and ask questions later. The goal is not to build a bot that is always active. The goal is to build one that knows when it has no edge.