The phrase “higher for longer” gets used like a weather forecast — as if the only question is when rates finally fall and the easy-money sky returns. That framing misses what actually changed. The important shift is not that rates went up; it is that the price of money stopped being zero and is unlikely to go back. When a dollar next year is once again worth meaningfully less than a dollar today, every investment is judged against a bar it did not have to clear for a decade. So “who wins” is the wrong question to ask about this era. The honest one is what a durably positive real rate does to how you value anything — and how to invest when nobody, including the Fed, actually knows how long it lasts.

The Hurdle Rate Is Back

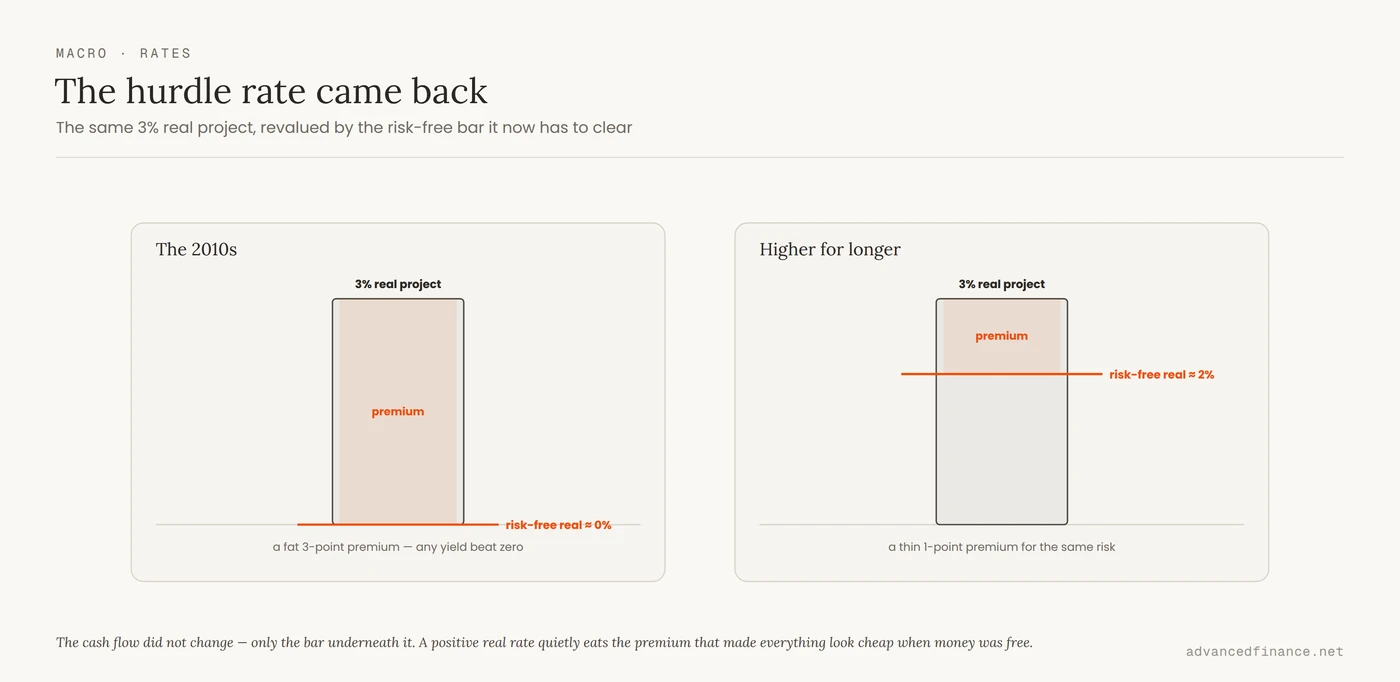

For most of the 2010s the risk-free rate sat so close to zero that it worked as no constraint at all: any project that might earn something beat the alternative of earning nothing. That is what a zero rate really is — the suspension of opportunity cost. A higher-for-longer world switches it back on. Today the 10-year real, inflation-adjusted Treasury yield sits near 2%, which means safe money now earns a genuine return after inflation, something it did not do for most of the prior decade. Every risk you take is measured against that return you could collect doing nothing risky at all. The hurdle rate — the return an investment has to clear to be worth its risk — is no longer a rounding error. It is the single most important number that came back, and it quietly reprices everything from a growth stock to a rental property to a no-cash-flow bet like bitcoin to your own emergency fund. To make it concrete: a venture promising a 3% real return looked irresistible in 2015, when safe money earned roughly nothing, so any yield beat the alternative; today, with about 2% real available for taking no risk at all, that same 3% is a wafer-thin one-point premium for real risk — the identical cash flow, repriced by the hurdle alone. The mechanics of exactly how a rate move flows through to prices belong to the way a rate change reprices assets by their duration; here the point is simpler and more permanent — the bar itself is back, and it is no longer near zero.

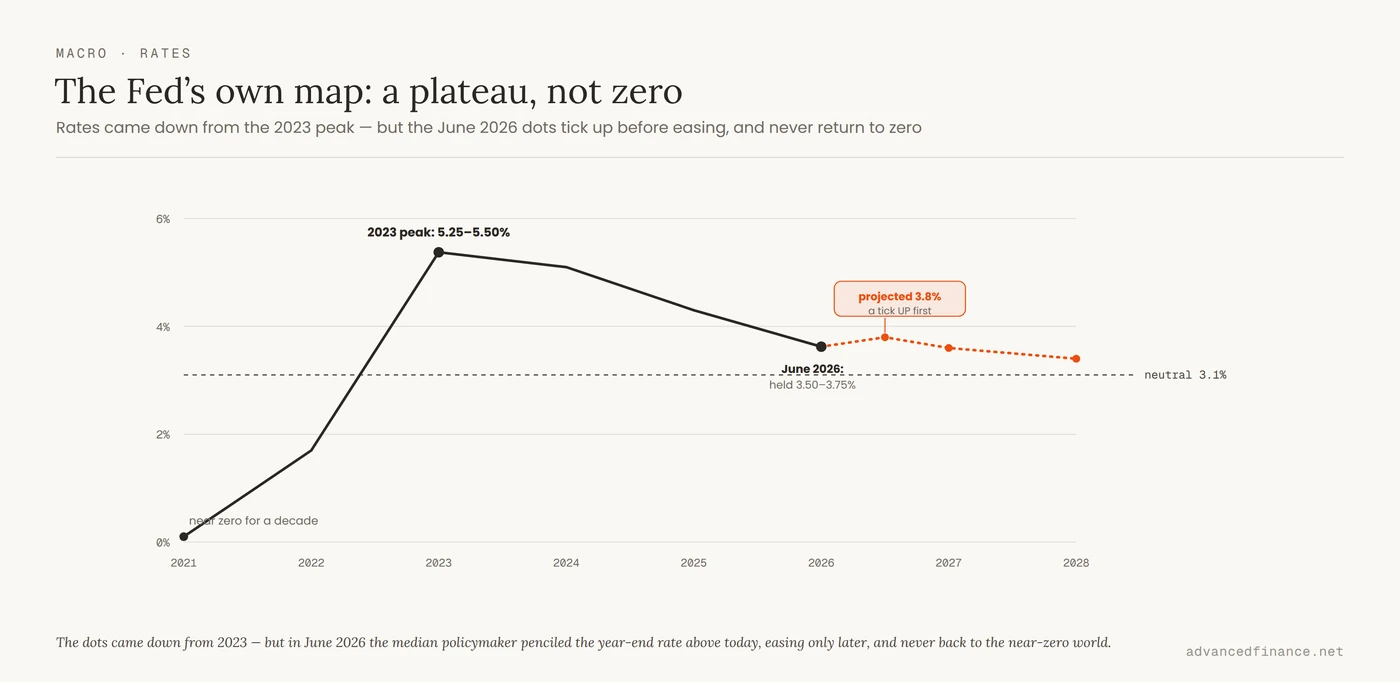

The Fed’s Own Dots

It is tempting to read elevated rates as a storm to wait out, but the Fed’s own projections say the opposite of a quick reprieve. At its June 2026 meeting the Fed held the target range at 3.50–3.75% and noted that inflation “remains elevated,” in part because of supply shocks — and the projections it released alongside were a hawkish revision, not a dovish one. In that Summary of Economic Projections the median policymaker put the funds rate at 3.8% at the end of 2026 — above where it sits today — which points to one more hike this year rather than a cut, after that 2026 dot was lifted from 3.4% just three months earlier as the median core-PCE inflation forecast jumped to 3.3% from 2.7%. Only further out does the median drift lower: 3.6% at the end of 2027, 3.4% at the end of 2028, toward a “longer-run” neutral rate of 3.1%. Even that glide is contested — the committee split almost evenly, with half the participants seeing the rate above roughly 4.1% and half at or below today’s level. Read honestly, the dots do not promise easing. They describe a plateau in the low-3s at best, a touch higher first — and, the one thing they agree on, no return to the near-zero world at all.

| Horizon | Median federal funds rate |

|---|---|

| Now (June 2026, held) | 3.50–3.75% |

| End of 2026 (projected) | 3.8% — above today |

| End of 2027 | 3.6% |

| End of 2028 | 3.4% |

| Longer run (neutral) | 3.1% |

Cash Became an Asset

The most underappreciated consequence is what the shift did to cash. For a decade, holding cash was a guaranteed slow loss — the reason “dry powder” felt like a drag and everyone reached for yield somewhere. With short Treasuries and bills now paying a real return, cash has quietly become a legitimate position rather than the residue of indecision. It earns while it waits, and it buys optionality: the ability to pick up assets from forced sellers without having to sell your own at the wrong moment. This is the rare gift of the regime — the boring, liquid, safe corner of a portfolio is finally being paid to exist. Sizing it on purpose, and treating cash as a genuine holding in the mix rather than an afterthought, is one of the few free improvements the era hands you.

The Zombie Cleanout

Cheap money did more than inflate valuations; it kept alive companies that could not pay their own way. Economists call them zombie firms — businesses whose operating profit does not cover their interest bill. The Bank for International Settlements, defining a zombie as a firm at least ten years old whose earnings have failed to cover its interest for three straight years, found the share of such firms across advanced economies climbed from about 2% in the late 1980s to roughly 12% by 2016, and estimated the long fall in interest rates explained around a sixth of that rise. A higher-for-longer rate takes the subsidy away: a business that survived only because money was free now has to justify itself or fail. But here honesty matters, because the doom version oversells it. The Federal Reserve’s own research, using a stricter test, puts US zombies at only about 10% of public firms and 5% of private ones and concludes they “are not a prominent feature of the U.S. economy”. So the cleanout is real but gradual — a slow tightening of the screws, not the mass extinction the headlines promise.

Nobody Knows the Length

Here is the part every confident “who wins” list skips: nobody knows how long this lasts, including the people who set the rate. The Fed’s dots are not a promise; they are a snapshot of guesses that shift every quarter, and they have been wrong in both directions for years. The June 2026 revision is the proof — in a single quarter the Fed’s own year-end-2026 estimate jumped from 3.4% to 3.8% as a supply shock pushed its inflation forecast up. If the people with the models and the votes can move their own year-end number by nearly half a point in three months, the odds that you can position a portfolio around the precise path are not good. Betting a portfolio on a specific path — piling into long bonds because you are sure cuts are coming, or shunning them because you are sure they are not — is just the mirror image of the mistake that defined the last cycle, when a decade of investors were certain rates “had to normalize” and were wrong for far longer than they could stay solvent. Conviction about the mechanism, that a positive real rate is a hurdle, is not the same as conviction about the timing, how high and how long. The first is durable. The second is a coin flip dressed as analysis.

Build a Book That Doesn’t Care

So the winning move is not to pick the era’s champions; it is to build a portfolio that does not need you to forecast the era at all. Keep bond duration short to intermediate, so a wrong guess on rates bruises you rather than breaks you. Favor businesses that fund their own growth from cash flow rather than the patience of lenders, because those are the ones indifferent to the refinancing calendar. Treat the risk-free yield as your hurdle: if an investment cannot plausibly clear the roughly 2% real you can now earn risk-free, plus a fair premium for whatever risk it carries, it is not cheap — it is just risky. And recognize that this same discount-rate arithmetic is what tilts the long contest between growth and value, and what strains the old stock-and-bond balance that leaned on ever-falling rates for its ballast. None of it requires knowing the future. It requires respecting that money, at last, has a price again.

And if you insist on a list of winners — the thing the title of every article like this promises — the honest one is unglamorous, and it falls straight out of the hurdle. The beneficiaries are whatever does not depend on cheap money: banks and lenders whose deposits and floating-rate loans reprice upward as rates hold high, short-duration income that keeps rolling into fresh yield, and cash-generative businesses that fund their own growth instead of borrowing it. Notice that these are all one idea wearing different labels — things that do not need rates to fall — which is why “who wins” and “how do I build a portfolio that doesn’t care” turn out to be the same question with the same answer.

FAQ

What does “higher for longer” actually mean?

Not that rates never fall, but that they settle well above the near-zero 2010s. The Fed held at 3.50–3.75% in June 2026 and, with inflation still elevated, projected the 2026 year-end rate slightly higher at 3.8% before any easing, drifting toward a 3.1% longer-run neutral. So the near-term risk is a touch higher, not lower — and either way, not a quick return to zero.

Is cash actually a good place to be now?

It is a legitimate position for the first time in years. Short Treasuries pay a real return, with the 10-year real yield near 2% after inflation, and cash gives you the optionality to buy when others are forced to sell. It is no longer a guaranteed slow loss — though that is an argument for holding it deliberately, not for making it your whole portfolio.

Will higher rates cause a wave of bankruptcies?

More a gradual tightening than a wave. Zombie firms are real, but the Federal Reserve’s own estimate puts them at high single digits of US firms and calls them “not a prominent feature” of the economy. The subsidy that kept weak businesses alive is being removed slowly, not slammed shut overnight.

Should I buy long-term bonds to lock in these yields?

Only with your eyes open to duration risk: if rates rise further, a long bond’s price falls hard, and nobody can reliably predict the path. Keeping duration short to intermediate lets you capture most of the yield without betting the portfolio on a forecast the Fed itself keeps revising.

How long will the higher-for-longer era last?

No one knows, including the Fed, whose projections move every quarter — in mid-2026 it revised its own year-end estimate up by nearly half a point in a single quarter. That uncertainty is precisely why the durable strategy is a portfolio built to be indifferent to the answer rather than one wagered on a particular rate path.

Author’s Insight

Over two decades of following rate cycles, the thing I had to unlearn was a reflex built up across the 2010s: that cash was trash and any yield, anywhere, was worth reaching for. That instinct made sense when the risk-free rate was zero. It is actively dangerous now that it is not. What changed my own portfolio most was almost embarrassingly simple — I started writing the risk-free yield at the top of every investment decision and asking whether the thing in front of me could really beat it once its risks were counted. A surprising amount of what looked attractive in the free-money years does not clear that bar. I also stopped trying to guess when the Fed pivots, because I have watched too many smart people get that exact call wrong for too long, and started building around the one thing I am sure of: money has a cost again, and that cost is the yardstick I hold everything against.

Bottom Line

“Higher for longer” is not a forecast to wait out; it is the return of the most basic force in finance — a positive real cost of money. The Fed held at 3.50–3.75% in June 2026 and, with inflation still elevated, penciled in a touch higher before any easing, settling toward a 3.1% neutral rate — so a genuine hurdle rate is back for years, and it reprices everything you own against roughly 2% you can now earn taking no risk at all. That makes cash a real asset again, slowly strips the subsidy from businesses that never earned their keep, and quietly favors the durable over the merely fast-growing. But the honest core is that no one knows how long it lasts — so the win is not a list of rate-regime champions. It is a portfolio built to shrug at the question: short duration, self-funding businesses, and every decision measured against the yield you no longer have to take any risk to earn.