Every guide to tax-advantaged accounts is a tour of the same vehicles — 401(k), IRA, Roth, HSA — recited with their contribution limits, as if picking the right account were the whole game. It isn’t. An account is just a wrapper: a rule about when, or whether, the government taxes what’s inside it. Two investors can hold the identical accounts and the identical funds and still end up with meaningfully different after-tax wealth, because the money is actually made in two decisions the brochures skip — which asset you put in which wrapper, and whether you choose to pay the tax now or later. This guide is about those two levers (with the current 2026 figures), because they, not the account names, are where the “net” in your net profit really comes from.

The Account Is Just a Wrapper

Strip away the acronyms and there are only three tax treatments in the entire system. Tax-deferred accounts — the traditional 401(k) and IRA — let you deduct the money going in and tax it coming out. Tax-free accounts — the Roth, and the HSA when used for medical costs — take money that has already been taxed (or never taxes it at all) and then let it grow and come out untouched. And taxable accounts offer no shelter but complete flexibility, plus the lower rates that apply to long-term gains. That is the whole toolkit. Knowing the three buckets is table stakes; every generic article stops there. The edge is in how you use them together, and the two mistakes that quietly cost the most are filling the buckets in the wrong order and putting the wrong assets inside them.

Fill the Buckets in Order

Before you agonize over which vehicle is best, get the sequence right, because sequence beats selection. First, capture the full employer match on your workplace plan — it is an instant, guaranteed return no market can promise, and leaving it unclaimed is the single most expensive tax mistake there is. Second, if you are eligible, fund a Health Savings Account, the only account that is tax-free on all three legs: IRS Publication 969 confirms HSA contributions are deductible, the earnings grow tax-free, and withdrawals for qualified medical expenses are not taxed (the 2026 HSA limit is $4,400 for self-only coverage and $8,750 for a family). Pay small medical bills out of pocket, let the HSA compound, and it quietly becomes a stealth retirement account. Third, max the main tax-advantaged accounts — for 2026 the IRS caps 401(k) salary deferrals at $24,500, with catch-ups of $8,000 from age 50 and $11,250 for ages 60–63, and IRAs at $7,500 (plus a $1,100 catch-up). Only then does the rest go into a taxable account — which is not a consolation prize but the most flexible bucket you own, and, used well, barely taxed at all.

Tax Now or Tax Later

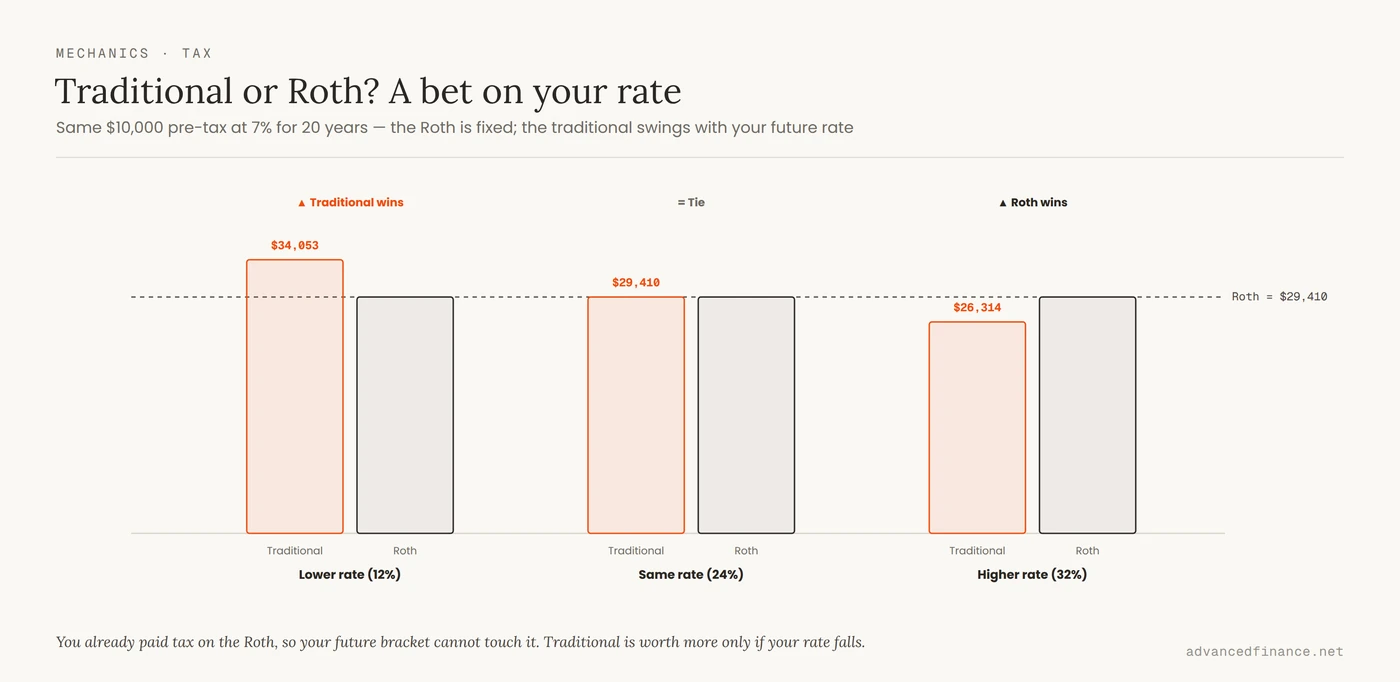

The traditional-versus-Roth debate is usually argued as if one answer were universally right. It isn’t a question of better; it is a question of when your tax rate will be higher. A traditional account deducts your contribution today and taxes the withdrawal in retirement, while a Roth takes after-tax money now and lets qualified withdrawals come out entirely tax-free. Put real numbers on it and the logic is stark: contribute the same pre-tax $10,000, grow it at 7% for 20 years, and the winner depends only on your future rate.

| Your tax rate in retirement | Traditional (net) | Roth (net) | Winner |

|---|---|---|---|

| Lower (12%) | $34,053 | $29,410 | Traditional |

| Same (24%) | $29,410 | $29,410 | Tie |

| Higher (32%) | $26,314 | $29,410 | Roth |

Notice that the Roth figure never moves — you already paid the tax, so your future bracket is irrelevant — while the traditional outcome swings entirely on a rate you can only guess at. That is the whole decision: a bet on your own future bracket. “Roth is always best” is a slogan, not analysis, and because almost nobody truly knows their future rate, holding some of each is a legitimate hedge. Two wrinkles hit higher earners. From 2026 the choice is partly removed by law: under the SECURE 2.0 Act, anyone whose prior-year wages exceeded $150,000 must make their 401(k) catch-up contributions as Roth, in after-tax dollars — the pre-tax option is simply gone for that slice. And direct Roth contributions phase out at higher incomes, though the “backdoor Roth” — contributing to a traditional IRA and converting it — remains a legal route around the cap.

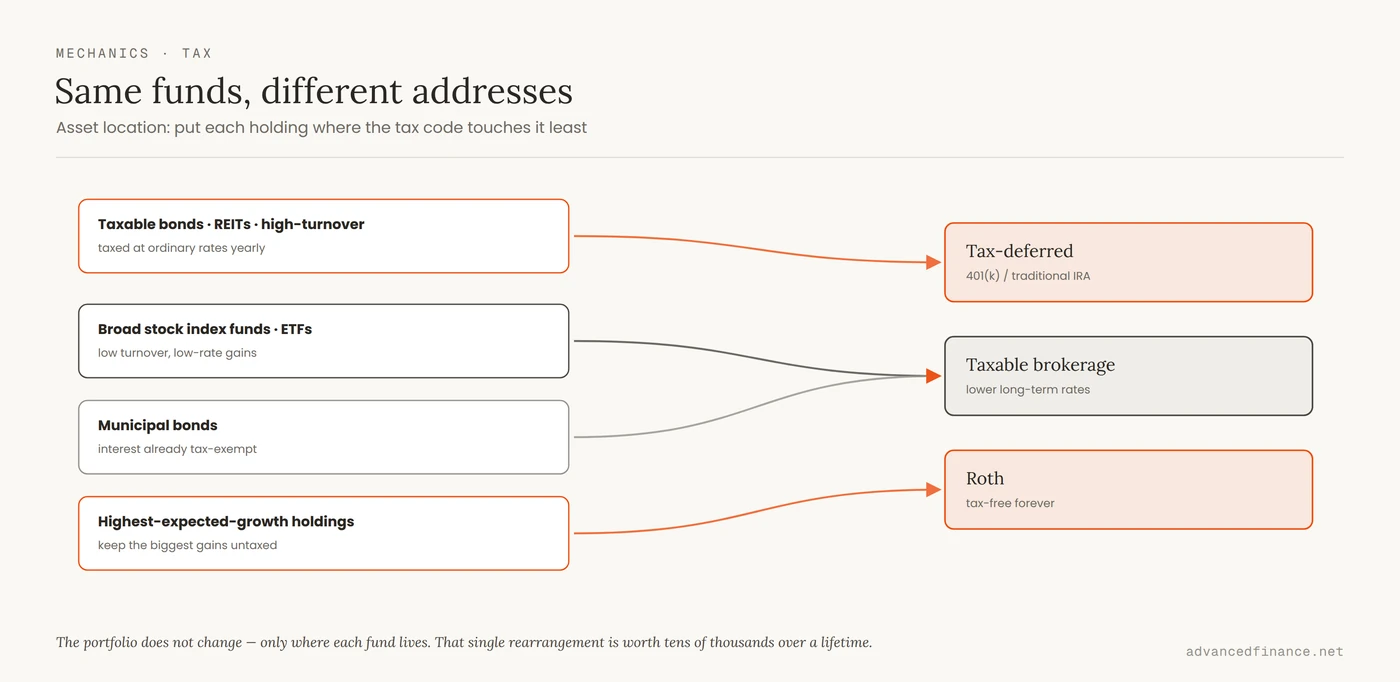

Asset Location, the Real Lever

This is the lever the account tours rarely dwell on, even though it is where much of the real after-tax money is made. Once your money is spread across taxable, tax-deferred, and Roth accounts, it matters enormously which asset sits in which one — and most investors throw the advantage away by mirroring the same stock-and-bond mix in every account. The fix, in Vanguard’s guidance, is to hold tax-inefficient assets — taxable bonds, REITs and high-turnover funds, whose income is taxed at ordinary rates — inside your sheltered accounts, and keep tax-efficient assets like broad stock index funds in the taxable account, where their long-term gains and qualified dividends are taxed at lower rates. Reserve the Roth, which is tax-free forever, for your highest-expected-growth holdings, so the largest gains are the ones that never get taxed. Nothing about the portfolio changes — the same funds, the same accounts — only their addresses. Vanguard estimates that doing this deliberately adds on the order of 0.05% to 0.30% a year, which in their example meant roughly $74,000 less tax over 30 years on a $1 million portfolio. Unspectacular per year, decisive over a lifetime.

| Asset | Why the tax code treats it this way | Best home |

|---|---|---|

| Taxable bonds, REITs, high-turnover funds | Income taxed at ordinary rates, yearly | Tax-deferred (traditional 401k/IRA) |

| Broad stock index funds / ETFs | Low turnover; qualified dividends & long-term gains taxed at lower rates | Taxable brokerage |

| Highest-expected-growth holdings | You want the biggest gains never taxed | Roth (tax-free forever) |

| Municipal bonds | Interest already federal-tax-exempt | Taxable (sheltering wastes the exemption) |

The Taxes You Don’t See

Three costs quietly erode returns, and none of them show up as a line you chose. The first is tax drag: in a taxable account, a fund’s own turnover and distributions can hand you a tax bill every year even if you never sold a share, and higher earners owe an extra 3.8% Net Investment Income Tax on top of their regular rate — which is exactly why a high-turnover active fund can be so much more expensive to hold there than a low-turnover index fund. The second is phantom income: REITs and some bond funds distribute income that is taxable even when you automatically reinvest it, so you owe tax on cash you never actually pocketed. The third is the one people forget entirely: a traditional account is tax-deferred, not tax-free. Your “$1 million” balance is really a million dollars minus a future tax bill, and required minimum distributions can later force money out and push you into a higher bracket — and higher Medicare premiums — whether you need the cash or not. Deferral is a loan from the government that you repay eventually, at a rate you do not control. Only the Roth and the HSA truly escape it.

Put It To Work

Turn the whole thing into an order of operations you run once and then automate:

- Take the full employer match before funding anything else — it is the highest guaranteed return available to you.

- Fund and invest an HSA if you are eligible, paying routine medical costs from cash so the account can compound untouched.

- Choose traditional or Roth by an honest view of your future tax rate — and split contributions if you genuinely can’t call it (remembering that high earners’ catch-ups must now go to Roth).

- Locate assets on purpose: tax-inefficient holdings in shelters, tax-efficient ones in taxable, highest-growth in the Roth.

- In the taxable account, use losses to offset gains through tax-loss harvesting, and rebalance in a tax-aware way so you are not realizing gains you didn’t have to.

- Let deeply appreciated assets ride where you can, since the step-up in cost basis at death can erase the embedded gain for your heirs entirely.

The rule underneath all of it: taxes are a cost to shave, never the reason you own something. A strong after-tax result still begins with a sound portfolio, which is why this sits on top of getting how your holdings fit together right in the first place. A large share of why most long-term investors underperform their own funds is not bad stock-picking; it is leakage, and tax is the leak you can plug with nothing more than paperwork and patience.

FAQ

Should I choose a Roth or traditional 401(k)?

It depends entirely on whether your tax rate will be higher now or in retirement. If you expect a higher rate later, the Roth is better; if you expect a lower one, the traditional is. Since most people can’t be certain, splitting contributions hedges the bet — though note that from 2026, if your prior-year wages topped $150,000, your catch-up contributions must go to Roth regardless.

Can I have both a 401(k) and an IRA?

Yes. You can contribute to both in the same year — for 2026, up to $24,500 in a 401(k) and $7,500 in an IRA — though the deductibility of your IRA contribution can phase out at higher incomes if you’re also covered by a workplace plan. The two accounts stack rather than compete.

What happens to my HSA if I never have large medical bills?

After age 65 you can withdraw HSA funds for any purpose and pay only ordinary income tax, exactly like a traditional IRA, while withdrawals for medical costs stay tax-free at any age. Before 65, non-medical withdrawals owe income tax plus a 20% penalty, which is precisely why the account is best left invested to compound.

Is asset location worth the effort for a small portfolio?

Less so at the very start, when everything may fit in one or two accounts and there is little to rearrange. Its value compounds as your balances grow across account types; once you hold meaningful sums in both taxable and sheltered accounts, placing each asset correctly is about as close to free money as investing offers.

Are ETFs more tax-efficient than mutual funds?

Generally yes. Their structure lets them avoid passing through many of the capital-gains distributions that mutual funds regularly trigger, so a broad-market ETF held in a taxable account usually creates noticeably less annual tax drag than a comparable actively managed fund. That makes ETFs a natural fit for the taxable side of an asset-location plan.

Author’s Insight

Over two decades of doing this, the pattern I keep seeing is that the investors who end up wealthiest are rarely the ones who found the best stock — they are the ones who were most disciplined about what they kept. I treat tax planning as a year-round habit rather than an April scramble, and the single change that did the most for my own results was embarrassingly boring: I stopped mirroring the same holdings in every account and started placing each asset where the tax code would touch it least. Automating the contributions helped too — money that never lands in the checking account is money you never feel you spent. None of it is clever. It just quietly compounds, and after enough years the tax you didn’t pay becomes one of the largest positions you own.

Bottom Line

Tax-advantaged investing was never really about collecting accounts; the account is only a wrapper that decides when the tax is due. The wealth is made in two decisions the checklists ignore: filling the buckets in the right order and then placing the right asset in each one, and betting the traditional-versus-Roth spread on an honest read of your future tax rate. Put the tax-expensive assets where the code can’t reach them, keep the tax-efficient ones where the low rates apply, respect that a deferred account still owes the government its cut, and let losses and the step-up in basis do their quiet work. Do that, and you shift your focus from the one number everyone watches — how much you earn — to the one that actually funds your life: how much you keep.