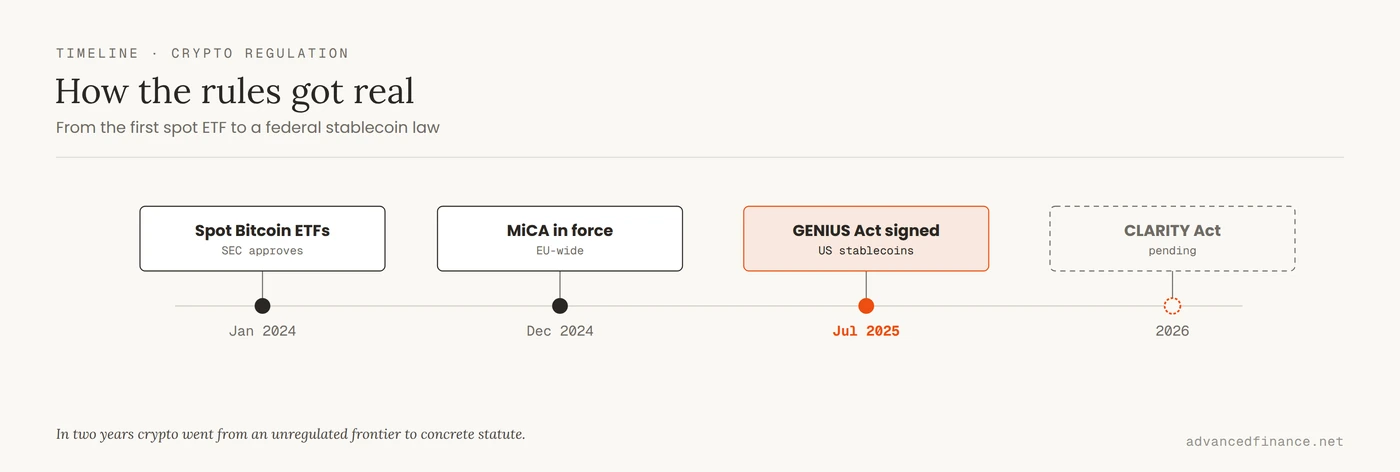

Ask a crypto investor about regulation and you usually hear a version of fear: that some agency is coming to ban it, tax it, or seize it. That framing is a decade out of date. By 2026 the rules are no longer a vague threat on the horizon — they are concrete law. The United States signed its first federal stablecoin statute, the GENIUS Act, in July 2025; the European Union’s MiCA regime has been fully in force since the end of 2024; and a US market-structure bill, the CLARITY Act, has passed the House and is moving through the Senate. None of this is abstract for an investor. Regulation is not a flood washing over the whole asset class at once. It is a filter, and it sorts your holdings by answering a small number of very specific questions. This guide covers the ones that actually touch your portfolio — and why the real danger is not regulation itself, but being caught on the wrong side of it while the rulebooks still disagree.

Regulatory status below is current as of mid-2026. This is one of the fastest-moving areas in finance, and several of these rules phase in over the following year, so treat the specifics as a dated snapshot rather than a permanent state.

A Filter, Not a Flood

Start by noticing who clear rules have actually helped. Regulation is what let BlackRock and Fidelity launch spot Bitcoin ETFs in early 2024 — institutions will not touch an asset with no legal footing, so clarity is what unlocked their capital. It is what now forces a stablecoin issuer to prove its reserves every month. And it is what steadily strangles the outright frauds that used to define the space; much of what you learn when you study the scams and rug pulls that clear rules are built to kill is simply what regulators are now codifying. For a holder, then, the threat is rarely “regulation exists.” It is far more specific: being the last person holding the token that gets reclassified, or sitting on the exchange that loses its license in your country. The filter is mostly cleaning the pool. The risk is being the thing it filters out.

None of this is costless, and it is worth being clear-eyed about the trade-offs. The same rules that legitimize the market also favor incumbents: licensing and reserve requirements are far easier for a large, well-capitalized issuer to meet than a small one, and the GENIUS Act’s ban on paying yield arguably protects banks more than savers. The pending CLARITY Act has critics too, including consumer advocates who argue it narrows the SEC’s protective reach. And compliance pressure inevitably squeezes smaller, permissionless projects that cannot afford a legal department. Clearer rules are mostly good for holders — but they are not neutral, and they are not free.

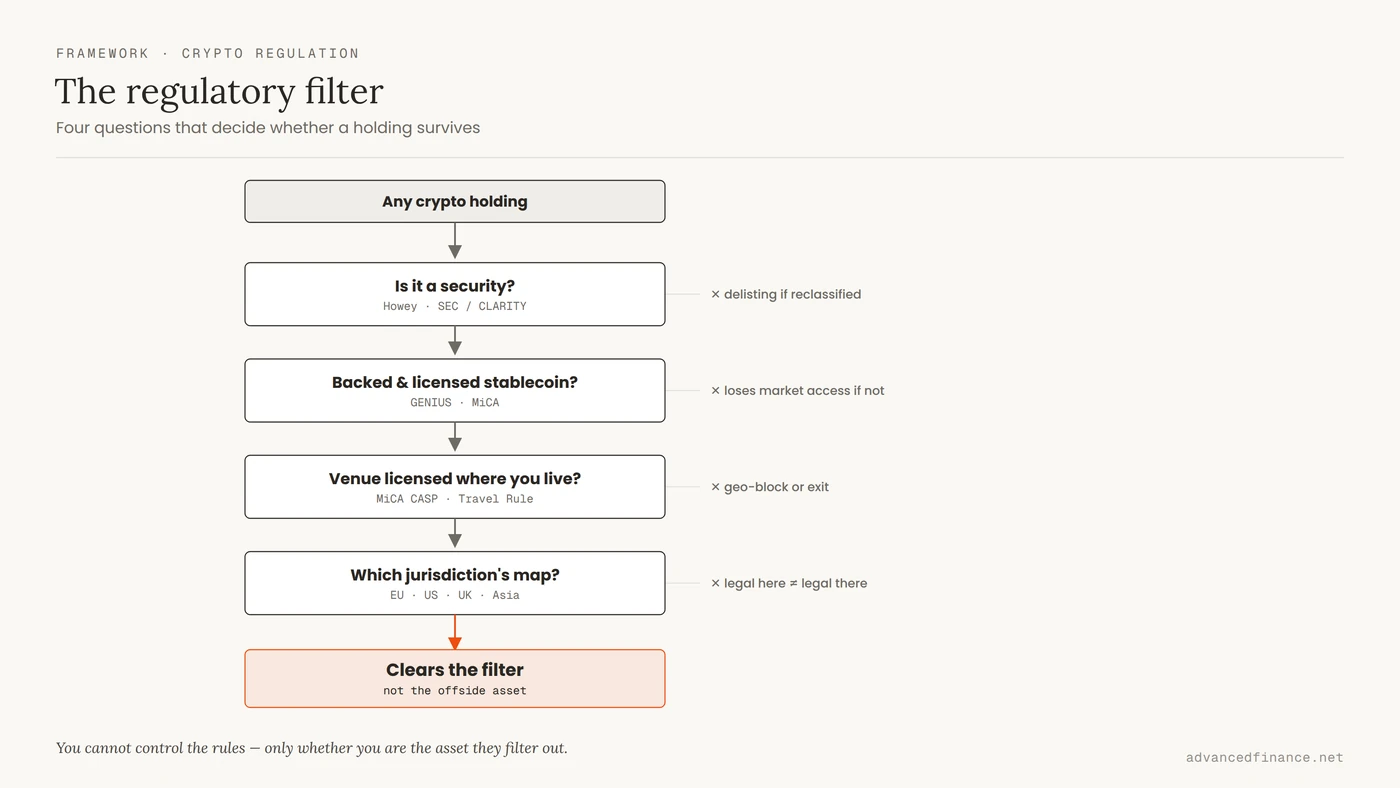

Is Your Token a Security?

In the United States this is the single most consequential question hanging over any token you own. Under the decades-old Howey test, if an asset is an “investment contract” — roughly, you put in money expecting profit from someone else’s effort — it is a security, and it must register with the SEC. When a token is deemed a security, US exchanges frequently delist it rather than carry the liability, which can strand holders almost overnight. This is not hypothetical: after the SEC’s 2023 lawsuits labeled tokens such as Solana, Cardano, and Polygon as securities, brokers including Robinhood delisted them, and it took a 2023 federal court ruling that XRP is not itself a security in exchange-market sales to lift that cloud from one major token. Bitcoin, by contrast, is broadly treated as a commodity rather than a security, which is part of why Bitcoin was treated as digital gold and got its ETF first; a great many smaller tokens still live in a gray zone. The CLARITY Act would finally draw the line — giving the CFTC authority over “digital commodities” and the SEC over securities, with a “mature blockchain system” test meant to move sufficiently decentralized assets out of the SEC’s reach — but until it is law, the classification is decided case by case, and the ambiguity itself is the risk.

Are Your Stablecoins Backed?

Here the law has moved from theory to hard requirement. The GENIUS Act now obliges a US payment-stablecoin issuer to hold reserves one-to-one in cash and short-term Treasuries, to publish the composition every month, and to be licensed — with non-bank issuers supervised by the Office of the Comptroller of the Currency. It also, notably, forbids issuers from paying you interest on the stablecoin itself — which is why yield-seeking capital has been migrating instead into tokenized money-market and Treasury funds. The EU’s MiCA imposes parallel demands on “e-money tokens.” The practical effect is a sorting: reserve-backed, licensed coins gain real legitimacy, while opaque or algorithmic ones face being squeezed out of regulated markets entirely — the 2022 implosion of the algorithmic stablecoin TerraUSD is exactly the failure these reserve rules are written to prevent. (These federal rules phase in over roughly a year, reaching full effect around 2026–27.) If you hold stablecoins, the question is no longer just “is it holding its peg” but “is the issuer licensed and the reserve genuinely there” — which is why it still pays to understand how a stablecoin actually holds its peg before you park money in one.

Who's Allowed to Hold Your Coins

Custody and access are the next filter. MiCA requires the platforms that trade or hold crypto for EU users — “crypto-asset service providers” — to be authorized, and GENIUS licenses stablecoin issuers. On top of that sits the FATF “Travel Rule”, which requires exchanges to attach your identity to transfers above roughly $1,000 and pass it to the receiving platform. In practice this means your exchange must be licensed where you actually live or it will geo-block you or withdraw — Binance’s staged retreat from several national markets is the visible version of this. Self-custody stays legal, but moving funds on and off regulated venues is increasingly identified rather than anonymous. This regulated-custody plumbing is also exactly what large allocators were waiting for — it is a recurring theme in why institutions needed regulated custody before they would move serious money on-chain.

The Maps Don't Agree Yet

The catch is that there is no single rulebook. Each major bloc is drawing its own map, and the seams between them are where the real investment risk lives.

| Jurisdiction | Framework | Stablecoins | Token classification |

|---|---|---|---|

| European Union | MiCA (in force) | Licensed e-money & asset-referenced tokens | Service providers authorized; broad coverage |

| United States | GENIUS (law) + CLARITY (pending) | Federal rules set, phasing in | Security-vs-commodity line still in flux |

| United Kingdom | FCA regime (phasing in) | Brought under FCA remit | Case-by-case; promotions already regulated |

| Singapore | MAS licensing | Regulated issuance | Licensing-based, selective |

| Hong Kong | SFC platform licensing | Regulated | Case-by-case; licensed hub |

A token or service that is perfectly legal in one place can be blocked in another, and the lines are still moving. Decentralized finance makes the fragmentation sharper still: when no company is in charge, regulators reach instead for the front-end websites, the developers, or the users, so the basic question of who is even responsible in decentralized finance remains genuinely unsettled. Betting your portfolio on a single jurisdiction’s interpretation holding is its own kind of risk.

What Actually Protects You

You cannot control the rules, but you can avoid being the asset they filter out. Use venues that are licensed in your own jurisdiction — a generic “regulated” badge is meaningless if the license is not valid where you live. Assume any token sitting in the security gray zone can be delisted, and do not over-concentrate in one such name. Prefer stablecoins whose issuer is licensed and whose reserves are disclosed, not just whichever advertises the highest convenience. Expect transfers above about $1,000 to carry your identity, and plan for it rather than around it. And keep clean tax records — not as compliance theater, but because the reporting net now closes automatically: US brokers must file the new Form 1099-DA on your disposals, and the international CARF and EU DAC8 frameworks push exchanges to share account data across borders. The through-line of every section here is the same: the danger was never regulation in the abstract, only being the last holder of something it rules offside.

FAQ

Is using DeFi illegal now?

No. Using decentralized protocols is not illegal in major markets. What is unsettled is responsibility: because no company sits in the middle, regulators increasingly target front-end interfaces, developers, and sometimes users. The compliance burden is shifting toward the individual, but the act of using DeFi is not banned.

Does the GENIUS Act make my stablecoin safe?

Safer, if the issuer is licensed and actually complies — it must hold one-to-one reserves and disclose them monthly. Two catches: the law bars issuers from paying you yield on the coin itself, and stablecoins that do not meet the standard may lose access to US markets. “Regulated” is not the same as “risk-free.”

Will my token be delisted if it’s called a security?

It can be. US exchanges often delist tokens deemed securities to avoid liability, which is the most direct regulatory risk to a specific holding. This is why concentration in a single ambiguous token is riskier than the token’s price chart alone suggests.

Do I have to use a KYC exchange?

For fiat on- and off-ramps and most regulated venues, yes. Self-custody remains legal, but the Travel Rule attaches your identity to transfers above roughly $1,000, so moving between regulated platforms is identified. Anonymity at the edges of the system is shrinking.

Should I move assets offshore to escape the rules?

Rarely wise. Tax-information sharing and enforcement now have long international reach, so “offshore” mostly adds counterparty and platform risk without actually escaping reporting. The jurisdictions worth caring about are the ones where you can legally and safely transact, not the ones that promise to hide you.

Author's Insight

The most useful shift in how I think about crypto regulation was to stop reading the headlines as weather and start reading them as a filter with a few specific settings. For years I watched people brace for a single apocalyptic ban that never came, while the changes that actually moved their money were quieter and narrower: a token quietly delisted after a classification call, a stablecoin issuer that could not meet reserve rules, an exchange that pulled out of a country overnight. Those are the events that hit a portfolio, and every one of them is foreseeable if you are watching the right four or five questions instead of the noise. I do not try to predict the politics anymore. I just try never to be the last holder of the thing that gets ruled offside.

Bottom Line

Crypto regulation in 2026 is no longer a looming threat; it is concrete law that mostly cleans up the market — killing scams, forcing stablecoins to prove their backing, and letting institutions in. For an investor it reduces to a handful of specific questions: is your token a security, are your stablecoins genuinely backed and licensed, who is allowed to custody your coins, and which jurisdiction’s map are you actually on. The GENIUS Act settled stablecoins, MiCA set the European standard, and the CLARITY Act will eventually draw the security line — but until every map agrees, the real risk is not regulation itself. It is holding the one asset, on the one platform, that ends up on the wrong side of it.