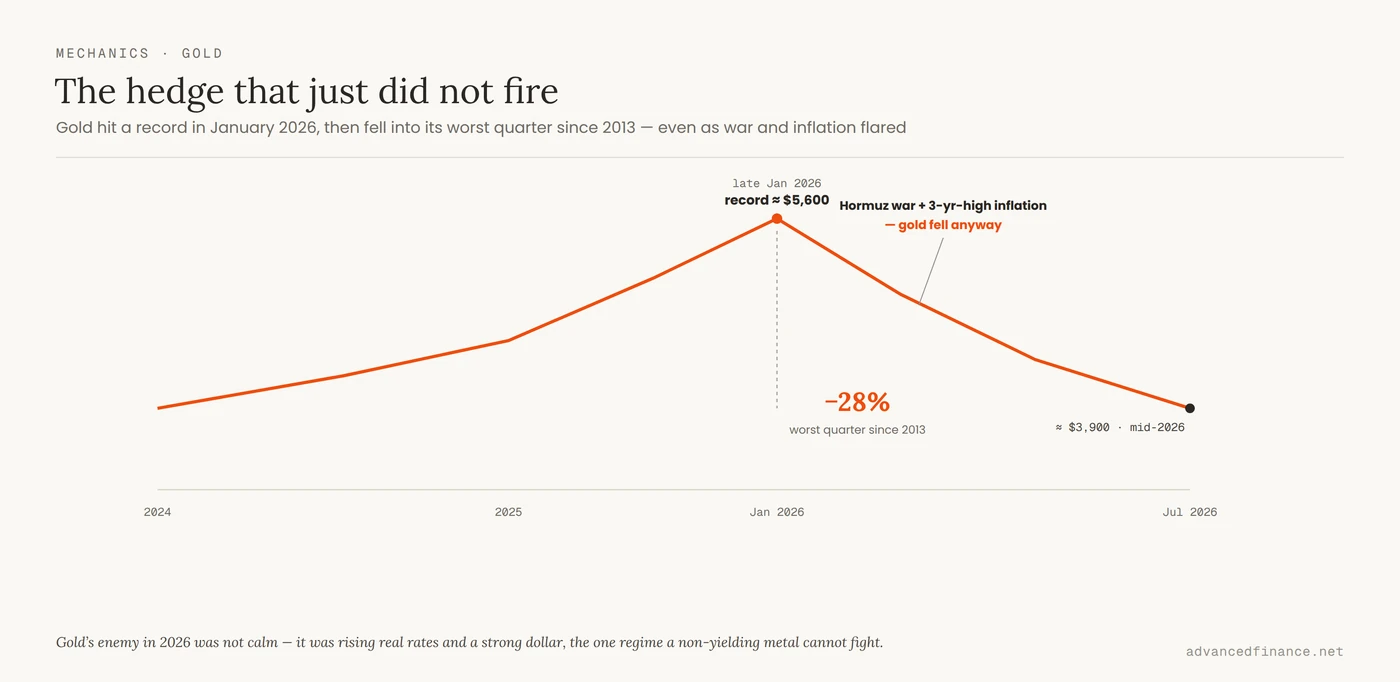

Gold spent late 2025 doing everything a haven is supposed to do, and then in 2026 it stopped. After touching a record near $5,600 an ounce in late January, it fell about 28% into the summer — its worst quarter since 2013 — even as a shooting war flared around the Strait of Hormuz and US inflation ran at a three-year high. If ever there were a moment for the ancient safe haven to fire, that was it. It didn’t. That is the honest starting point for anyone weighing gold against its self-styled digital successor, because it exposes the thing both camps get wrong: a hedge is not a permanent property of an asset. It is conditional on the regime, and 2026 is a live demonstration of what gold does and does not protect you from. This is not the deeper question of whether bitcoin is really digital gold — it is the prior question most comparisons skip: whether even real gold is the unconditional hedge it is sold as.

The Hedge That Just Didn’t

The facts are unusually clean because the test was so direct. Through the first half of 2026 the world served up exactly the conditions gold is supposed to thrive in — geopolitical shock, revived inflation fear, a Strait-of-Hormuz crisis — and gold fell anyway. Morgan Stanley framed it plainly as a reality check on gold’s safe-haven status, and the World Gold Council itself acknowledged questions about gold’s muted response to the conflict. This matters more than any five-year backtest, because it is the rare case where the story was tested in real time and came back ambiguous. The lesson is not that gold is broken. It is that “gold protects you when confidence cracks” is too simple: it protects you against some cracks and not others, and which is which depends on what else is happening to interest rates and the dollar at the same time.

Why Gold Actually Fell

The mechanism is not mysterious. Gold pays no interest, so its single biggest rival is the real, inflation-adjusted yield on cash and bonds — and in 2026 that yield rose. A hawkish Federal Reserve signaled it was not done raising rates, real Treasury yields climbed toward the mid-4% range, and the dollar strengthened. Each of those is direct poison for a non-yielding asset priced in dollars: when safe cash pays a healthy real return, the opportunity cost of holding a metal that yields nothing goes up, and money that might have hidden in gold hid in the dollar and short-term Treasuries instead. That is why the Middle East scare did not lift gold — the safe-haven bid that did exist flowed to the currency and to real yield, not to bullion. Gold’s enemy in 2026 was not calm; it was competition from cash that finally pays a positive real return again.

What Gold Really Hedges

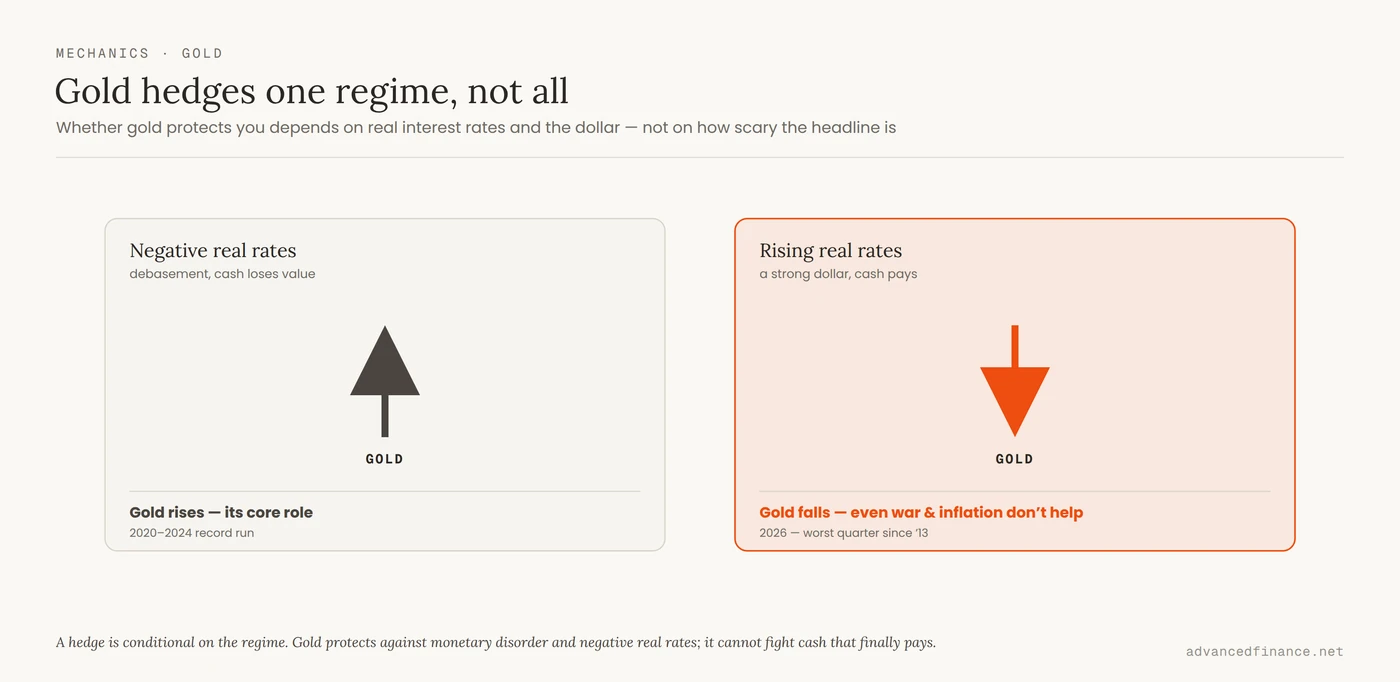

Put those together and gold’s real job comes into focus, narrower and more reliable than “inflation hedge.” Gold is protection against monetary disorder and negative real rates — against a world where currencies are being debased faster than savers are compensated, where cash loses purchasing power and there is nowhere safe to earn a real return. In those regimes gold shines, which is exactly the environment that drove its 2020–2024 run. But when the central bank is fighting inflation by pushing real rates up rather than letting them go negative, that same force works against gold. So the honest framing is not “is gold a good inflation hedge” but “which inflation regime are we in” — the same regime-dependence that governs whether any hedge actually works when a shock hits. A hedge that only works in some regimes is still valuable. It is just not the all-weather shield the marketing implies.

| Regime | What gold tends to do | Recent example |

|---|---|---|

| Negative real rates, debasement fear | Rises — its core role | 2020–2024 record run |

| Rising real rates, strong dollar | Falls despite inflation | 2026, worst quarter since 2013 |

| Acute crisis while real rates rise | Muted; the bid goes to cash | 2026 Hormuz flare — fell anyway |

| Growth-scare recession | Usually firm as rates fall | Classic haven behavior |

The Record Still Stands

None of this cancels gold’s long case; it sharpens it. The structural bid is real and was not built on a single good year. Central banks bought more than 1,000 tonnes of gold in each of 2022, 2023 and 2024 — three record years running — and while 2025 cooled to 863 tonnes, that was still far above the roughly 473-tonne annual average of the 2010s, and the Council’s survey found 95% of central banks expect global reserves to keep rising. The institutions that issue the currencies gold hedges against are still accumulating it, just at a calmer pace. That is the difference between a price and a franchise: the 2026 drawdown is a price move driven by real rates, while the multi-year, multi-central-bank demand is a slower story about diversifying away from the dollar that a bad quarter does not undo. Hold gold for the franchise, and you can sit through the price.

Then Digital Gold Is Weaker

Here is where the comparison finally pays off. If even gold — with five thousand years of history and the world’s central banks as buyers — is only a conditional hedge that just failed a live test, then an asset that merely copies gold’s scarcity while trading like a risk position is on far weaker ground as “protection.” Bitcoin shares the one property (fixed supply) and none of the behavior: in the 2022 inflation shock it fell by roughly two-thirds while gold held roughly flat, and routing it through ETFs and institutional desks has only tied it more tightly to risk markets, not less. Whatever bitcoin is — and it may be a genuine bet on a new financial system — it is not a more reliable haven than the metal that itself just proved how conditional havens are. The scarcity story is the same for both; the behavior, which is what a hedge is actually judged on, is not.

How To Hold a Hedge Honestly

The practical takeaway is to demote both assets from “shield” to “tool with conditions.” Own gold, if you own it, as regime-dependent insurance — a modest allocation that earns its place in debasement and negative-real-rate worlds, held in the full knowledge that a rising-real-rate regime will hurt it, and never expected to fire on cue in every crisis. Remember it costs money to hold: no yield, plus storage, plus a US tax code that treats physical bullion as a collectible taxed up to 28%, above the top rate on ordinary long-term gains. Treat digital assets, if you want them, as speculation sized for the risk sleeve, never smuggled into the safe bucket under the label “digital gold.” And decide how much of each the way you decide any allocation — as a question of what role each holding plays and what it is correlated with, not as a slogan. The investor who knows exactly which regime their hedge needs is far safer than the one who thinks they own a shield.

FAQ

Why did gold fall in 2026 if inflation was high?

Because the Federal Reserve was fighting that inflation by keeping real interest rates high, and gold pays no yield. When real returns on cash and bonds rise and the dollar strengthens, a non-yielding metal becomes less attractive, so gold fell into its worst quarter since 2013 despite high inflation and a live geopolitical crisis.

Is gold still a safe haven?

Conditionally. Gold protects against monetary disorder and negative real rates, which is why it ran to records into 2024, but it is not an all-weather shield. In 2026 it fell even as war flared in the Middle East, because rising real rates and a strong dollar overwhelmed the safe-haven bid. A hedge that works in some regimes and not others is still useful, just not unconditional.

Is gold or bitcoin the better inflation hedge?

Gold has the far stronger claim, but the honest answer is that neither is unconditional. Gold at least has a long record and central-bank demand behind it; bitcoin shares gold’s scarcity but trades as a risk asset and fell about two-thirds in the 2022 inflation shock. If even gold’s hedge is regime-dependent, bitcoin’s is more so.

Are central banks still buying gold?

Yes, though at a calmer pace. After three straight years above 1,000 tonnes, central-bank buying cooled to 863 tonnes in 2025 — still far above the 2010s average of roughly 473 tonnes — and surveys show most central banks expect to keep adding. The structural move to diversify reserves away from the dollar has outlasted the 2026 price drawdown.

How much of a portfolio should be in gold?

There is no universal number, because it depends on the role you want it to play. Gold typically works as a small, stabilizing allocation held as regime-dependent insurance, not a large bet expected to drive returns. The key is sizing it for the specific job — protection in debasement and negative-real-rate regimes — rather than treating it as protection against everything.

Author’s Insight

The most useful thing 2026 taught me is that I had been lazy about the word “hedge.” For years I told myself gold was my protection when things went wrong, and then things went genuinely wrong — war, an inflation scare — and my hedge fell 28% because the one variable I had underweighted, real interest rates, moved against it. That was not gold failing; it was me holding a regime-dependent tool as if it were unconditional. I still own gold, and I still believe in the central-bank story that underpins it, but I now hold it with a condition attached: it is insurance against a debasement world, and in a rising-real-rate world it will hurt, and that is fine as long as I sized it knowing that. The same discipline is why I keep my digital assets in a completely separate mental box labeled “bet,” not “haven.” The costliest word in investing is a noun like “hedge” used without the conditions that make it true.

Bottom Line

Gold and digital assets get compared as rival hedges, but 2026 exposed the flaw underneath the whole debate: even gold is only a conditional hedge. It touched a record near $5,600 in January, then fell about 28% into its worst quarter since 2013 — and pointedly did not rally when war flared around Hormuz — because rising real rates and a strong dollar are the one environment a non-yielding metal cannot fight. Gold’s real, durable job is protection against monetary disorder and negative real rates, backed by a genuine multi-year central-bank bid that cooled but did not end. If that all-weather reputation cracks for gold, it certainly does not hold for “digital gold,” which copies gold’s scarcity but trades like a risk asset. Own each for what it actually does: gold as regime-dependent insurance, digital assets as sized speculation, and neither as the unconditional shield the marketing sells.