Tax-loss harvesting turns a paper loss into a real tax deduction. You sell an investment that has fallen below what you paid, use the realized loss to cancel out capital gains elsewhere, and stay invested by buying something similar but not identical. Done consistently, it can quietly add to your after-tax return for years. Done carelessly, it triggers the wash-sale rule, wastes the deduction, and creates a bookkeeping mess. This guide covers how it actually works, what it is genuinely worth (with real numbers, not the usual hand-waving), and the 2026 rule that makes crypto unusually efficient to harvest.

How Tax-Loss Harvesting Works

When an investment's market value drops below its cost basis, selling it "realizes" a capital loss. That loss first offsets your capital gains dollar for dollar; if losses exceed gains, you can deduct up to $3,000 against ordinary income each year, and carry the rest forward indefinitely. The rules for all of this live in IRS Topic No. 409.

A simple example. You bought 100 shares of an EV startup at $150 and it now trades at $100 — a $5,000 unrealized loss. Separately, you sold Apple this year for a $5,000 gain. By selling the EV position, you realize the $5,000 loss, it cancels the $5,000 Apple gain, and your net taxable capital gain becomes zero. Instead of paying 15% or 20% long-term capital gains tax on that Apple profit, you keep the cash and immediately reinvest in a similar (but not "substantially identical") asset so you never leave the market. The loss is banked; your exposure is intact.

The single biggest mistake is treating this as a December chore. The best harvests come from sharp intra-year drops — a year like 2022, when rising rates dragged down both stocks and bonds at once, handed disciplined harvesters losses they could carry forward for years. Wait until year-end and those moments are gone. There is still a hard deadline, though: for a loss to count in a given tax year you must sell by the last trading day of December — the loss is recognized on the trade date — so leave a buffer rather than trading in the final minutes.

What It's Actually Worth

Most articles tell you harvesting "adds about 1% a year." The honest answer is more nuanced, and the nuance is the whole point.

Vanguard's 2024 research put the "TLH alpha" — the extra annual after-tax return from harvesting — between 0.47% and 1.27%, rising with both net worth and discipline. But two caveats matter more than that headline range. First, those figures apply only to the taxable-equity slice of a portfolio; scaled across everything you own, the benefit shrinks fast — a mass-affluent investor with 25% of assets in taxable equities sees roughly 0.12% at the total-portfolio level, not 0.47%. Second, sloppy execution collapses it: Vanguard found investors who harvested suboptimally captured as little as 0.04% to 0.13%. Independent academic work agrees the effect is real — a Financial Analysts Journal study by Chaudhuri, Burnham, and Lo measured a long-run US average on the order of 1% a year — but the practical takeaway is blunt. Harvesting is worth real money only if you have a meaningfully taxable equity book and you do it consistently. On a small or mostly tax-sheltered portfolio, the juice may not be worth the squeeze.

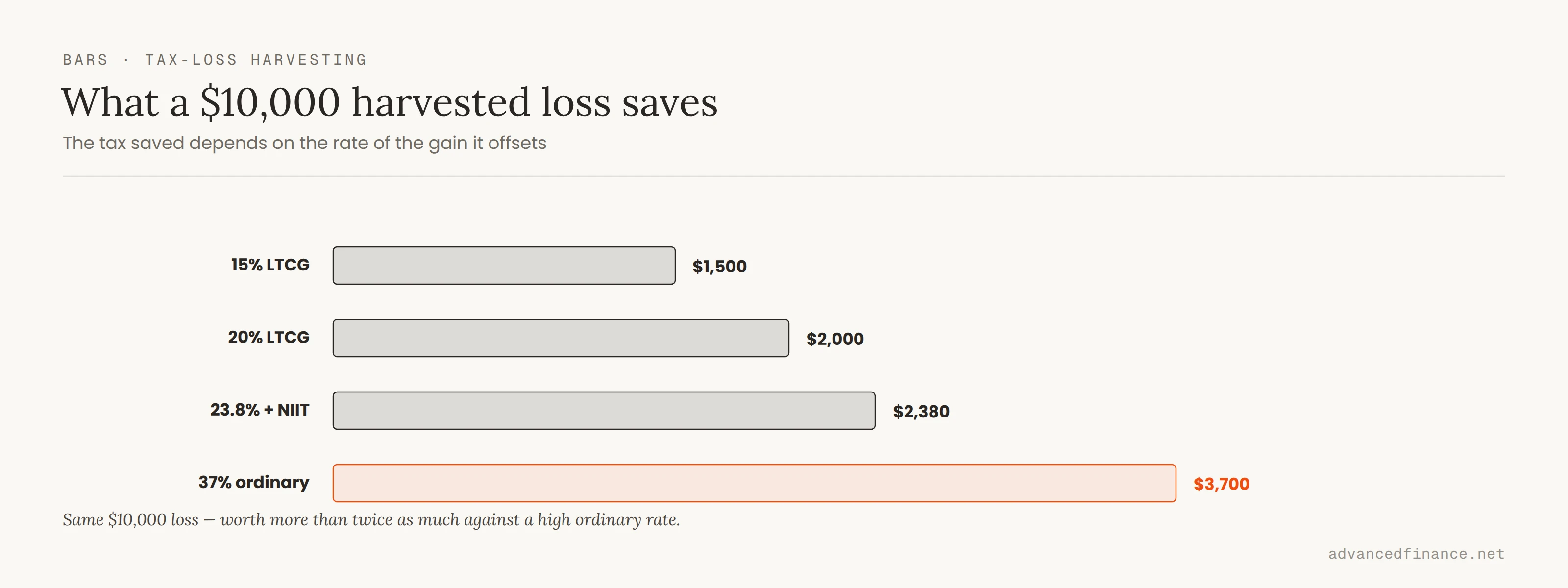

It also helps to see what a single harvested loss is worth in dollars, which depends entirely on the rate of the gain or income it cancels:

| A $10,000 harvested loss cancels… | Taxed at | You save |

|---|---|---|

| A long-term capital gain | 15% | $1,500 |

| A long-term gain, top bracket | 20% | $2,000 |

| A long-term gain + NIIT (high earners) | 23.8% | $2,380 |

| A short-term gain or ordinary income | up to 37% | up to $3,700 |

The type of gain matters, because losses net against the same category first. A loss that cancels a short-term gain — taxed at ordinary rates up to 37%, plus the 3.8% Net Investment Income Tax for high earners — is worth far more than one canceling a long-term gain, so prioritize harvesting against your most heavily taxed gains. (The $3,000 annual limit applies only when losses offset ordinary income, not when they offset capital gains.)

The Wash-Sale Rule

The wash-sale rule is the trap that catches DIY harvesters. If you sell a security at a loss and buy the same or a "substantially identical" security within 30 days before or after the sale — a 61-day window in total — the IRS disallows the loss for that year. The authoritative source is IRS Publication 550.

The subtlety most people miss is that the rule applies at the household level, across accounts. If you sell a stock at a loss in your taxable account but your spouse buys the same stock in their IRA — or your own robo-advisor rebuys it in another account — within the window, the loss is still disallowed. This is why coordinating harvesting with your tax-advantaged accounts and your spouse's holdings matters: the IRS looks through the legal entities to the economic reality.

To stay invested during that 30-day window, you buy something correlated but not substantially identical — and one subtlety is worth getting right. Swapping one S&P 500 fund for another provider's S&P 500 fund (say VOO for IVV) tracks the identical index and sits in a genuine gray area, since the IRS has never defined "substantially identical." The conservative move is to switch to a different index that still fits your allocation.

| Sell to harvest the loss | Buy instead (different index) | Keeps you exposed to |

|---|---|---|

| S&P 500 fund (e.g. VOO) | Total US market (VTI) or Russell 1000 | US large-cap |

| Innovation/growth ETF (e.g. ARKK) | Nasdaq-100 (QQQ) | US growth & tech |

| A single stock | A sector ETF for that stock's sector | Sector exposure |

| Aggregate bond fund (e.g. BND) | A different-index bond fund | US investment-grade bonds |

Keep a written "replacement list" ready before you need it. When the market drops, you should already know your Plan B for every core holding, so you can harvest the loss and re-enter the same day rather than researching substitutes while the rebound runs away from you.

Crypto: The TLH Loophole

Here is where 2026 gets interesting. The wash-sale rule is written to cover "stocks and securities." The IRS treats cryptocurrency as property, not a security — so, as of the 2026 filing season, the wash-sale rule does not apply to crypto.

The practical consequence is large. You can sell Bitcoin or Ether at a loss to bank the deduction and rebuy the same coin the very same minute — no 30-day wait, no imperfect substitute, no gap in your position. That makes crypto the single most efficient asset for harvesting: you capture the loss without ever giving up your exposure or reaching for a proxy. In a volatile year, a crypto holder can harvest the same position repeatedly as it dips and recovers, in a way an equity holder simply cannot.

Two honest caveats. Congress has repeatedly proposed extending the wash-sale rule to digital assets, so this is a live opportunity that could close — possibly with little warning. And every sale is still a taxable disposal that resets your holding period and cost basis, so meticulous lot records are non-negotiable. Treat it as a genuine edge for now, and confirm your position with a tax professional before leaning on it hard.

Specific-Lot Selection

If you have bought the same asset over time — through dollar-cost averaging, say — not all your shares have the same cost basis. Most brokerages default to "First In, First Out," which sells your oldest, often cheapest shares first and produces a smaller loss. Switching your cost-basis method to "Specific Identification" lets you sell the exact high-cost lots that generate the largest realized loss.

Suppose you hold 300 shares bought in three batches: 100 at $60, 100 at $90, and 100 at $120, with the price now at $70. Sell the $120 lot and you harvest a $50-per-share loss ($5,000); let FIFO sell the $60 lot and you book a $10-per-share gain instead. Same position, opposite tax outcome. This is also where harvesting overlaps with disciplined rebalancing without overpaying in taxes — you can trim overweight lots and capture losses in the same trade. One practical note: set your cost-basis method to Specific Identification before you sell — your brokerage may label it "Specific Shares," "Specified Lots," or "SpecID" — because you generally cannot reassign the lot after the trade settles.

Common Mistakes

- Letting the tax tail wag the investment dog. If your replacement asset materially underperforms the one you sold, you can lose more in return than you saved in tax. Only harvest when you have a substitute you are genuinely happy to hold.

- Ignoring transaction costs. On illiquid small caps or high-spread funds, commissions and bid-ask spreads can eat the benefit. If the tax saving is $200 but the round-trip costs $80, the effort may not be worth it.

- Tripping the qualified-dividend clock. Selling around an ex-dividend date can break the 61-day holding requirement and push your dividends from the lower qualified rate to ordinary income. Check the dividend calendar before harvesting in the back half of the year.

- Forgetting automatic reinvestment. A dividend reinvestment plan (DRIP) that rebuys the same fund within the 61-day window is one of the most common accidental wash sales. Switch off auto-reinvest on a position before you harvest it.

- Harvesting for its own sake. The goal is a lower lifetime tax bill, not a bigger loss count. A harvest that damages your allocation is not a win.

FAQ

Can I harvest losses in my 401(k) or IRA?

No. Tax-loss harvesting only works in taxable brokerage accounts. Gains and losses inside a 401(k) or Roth IRA are not taxed year to year, so there is no realized loss to harvest and nothing to offset against gains elsewhere.

How much can my losses actually offset?

Capital losses offset capital gains without limit — a million in losses can cancel a million in gains. Beyond that, you can deduct up to $3,000 of leftover loss against ordinary income each year and carry the remainder forward indefinitely, per IRS Topic 409. There is no expiration on carried-forward losses.

Does the wash-sale rule apply to crypto?

As of the 2026 filing season, no. The wash-sale rule covers "stocks and securities," and the IRS treats crypto as property, so you can sell a coin at a loss and rebuy it immediately. Legislation to close this has been proposed repeatedly, so treat it as subject to change and confirm with a tax professional.

What counts as "substantially identical"?

The IRS has never defined it precisely, which is why the safe path is to switch to a different index rather than another provider's version of the same one. Selling one S&P 500 fund and buying a total-market or Russell 1000 fund is widely treated as safe; swapping two S&P 500 funds is a gray area.

When should I not harvest at all?

When the costs outweigh the benefit: a small or mostly tax-sheltered portfolio, high transaction costs, no realistic near-term gains to offset, or no substitute you actually want to hold. Harvesting is a tool, not an obligation.

Author's Insight

In years of managing taxable portfolios, I have found the investors who win at this treat taxes as a variable cost to be managed, like fees — not as an afterthought in late December. But I have also watched people talk themselves into bad trades chasing a deduction. My rule is simple: I never harvest a loss unless I would be comfortable holding the replacement for the next five years, and I keep a standing replacement list so I am executing, not researching, when the market drops. The tax saving is the bonus. Staying invested in something I actually want to own is the point.

Bottom Line

Tax-loss harvesting is a year-round discipline, not a year-end scramble. Understand the wash-sale rule and coordinate it across your household, use specific-lot selection to maximize each loss, keep a replacement list so you never leave the market, and be honest about the magnitude — it pays off mainly on a meaningfully taxable equity book, done consistently. And in 2026, if you hold crypto, you own the most efficient harvesting asset there is, at least until the rules catch up. Everything here is US federal treatment — state taxes and non-US regimes differ — so review your positions for anything trading below cost, and fold these tactics into a broader plan with a tax advisor.